The United States Department of Veterans Affairs provides various benefits to active-duty service members and veterans, including the potential to buy a home with a VA mortgage. The VA loan offers an eligible veteran the chance to buy a home with low closing costs and no down payment, making the overall purchase more affordable than a conventional loan. However, the property you consider for a VA loan must meet the VA’s Minimum Property Requirements for a mortgage.

VA Home Loans 2024

So what kind of home loans is the VA offering in 2024? The specific loan amount and interest rate will depend on the situation. The loan limit also depends on certain factors. If you have full entitlement, there is no limit on loans over $144,000. If you have remaining entitlement, then your loan limit is based on the loan limit of your county.

VA Minimum Property Requirements Homebuyers Should Know

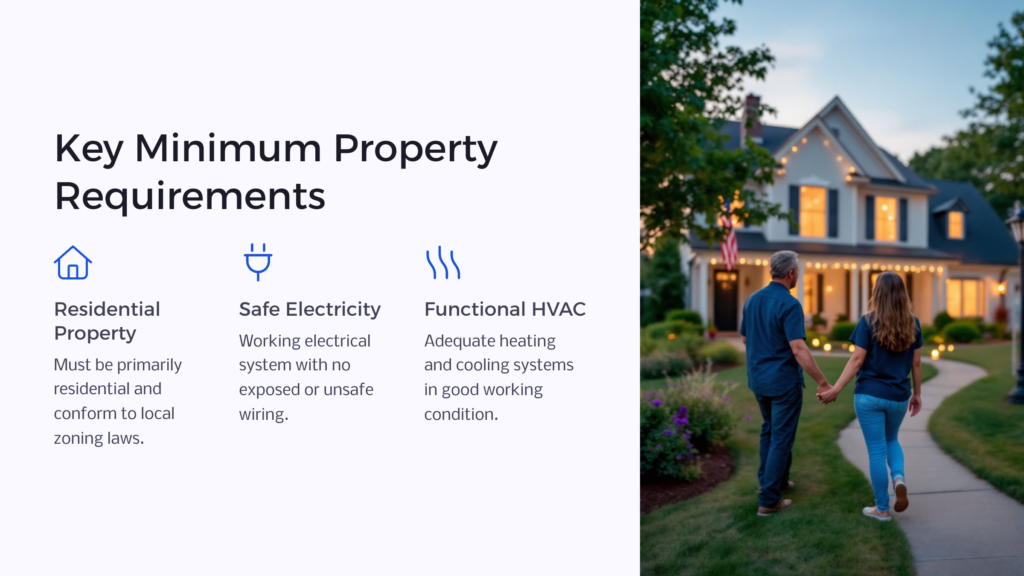

- Property is residential

- Working electricity

- No exposed wiring

- Functional heating and cooling system

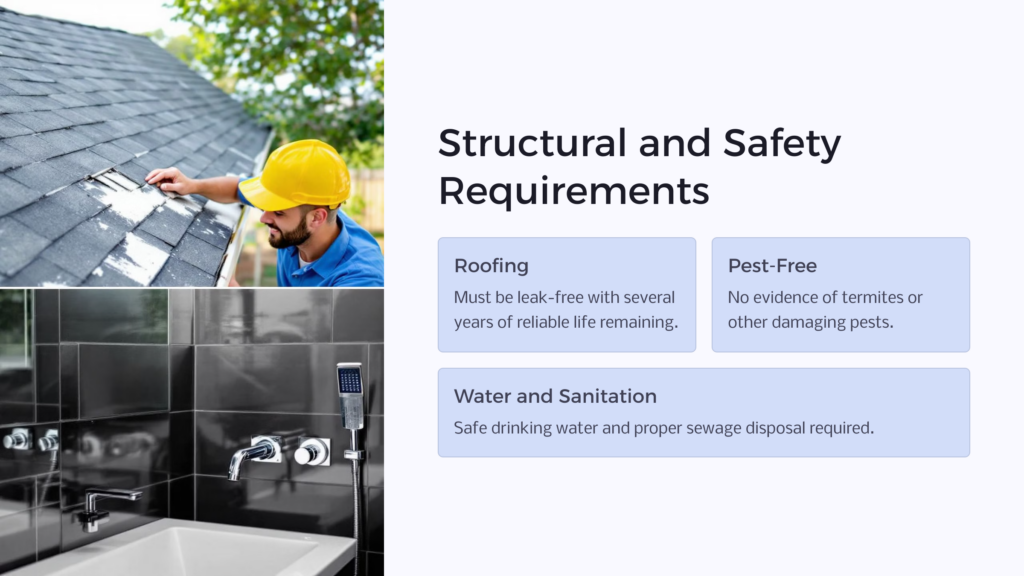

- Adequate roofing

- Structure is free from termites and other pests

- Proper water and sanitation

- Walls free from mold

- Proper drainage and free from water damage

- Accessible property year-round

- Free from lead-based paint

- Sufficient living space

- Accessible attic and crawlspace

The VA loan process helps veterans afford a home using their VA eligibility for benefits. The VA mortgage loan goes through an approved VA lender, and the VA guarantees the loan. As the guarantor, the VA imposes minimum property standards that the home must meet for VA eligibility.

Your lender will order an appraisal some time during the loan application process. A VA approved appraiser will conduct the appraisal on your home and check that it meets property requirements the VA imposes on all potential VA-backed loans. If your home doesn’t meet the VA’s Minimum Property Requirements, you can pay to make repairs so it will pass, or you can walk away from the house.

What Are VA Minimum Property Requirements?

When you apply for VA home loans, your loan application is subject to meeting the requirements of a mortgage through the VA. The VA guarantees these loans, meaning that they back them to prevent risk to the lender if you are unable to or do not pay your mortgage. One of the most critical VA loan requirements is that the home buyer must have an appraisal completed by an approved VA appraiser before your loan officer can approve your loan.

Like an FHA loan, a VA loan appraisal will look for specific features of a home. The VA refers to these features as Minimum Property Requirements, or MPRs, for short. The VA appraisal is more than just an assessment of your home to determine its real estate value; it also acts as a basic inspection to ensure that the home is safe, sound, and sanitary. This is where the MPRs come into play. Minimum Property Requirements can help the VA and your VA approved lender decide if a VA home loan should help you pay for the house you’ve chosen.

The VA includes the VA appraisal requirement to protect both its and your investment. Some homebuyers confuse the VA appraisal with a home inspection, but the two aren’t the same. Although the appraisal does check that the home meets Minimum Property Requirements, the appraiser won’t conduct a thorough inspection. If you want a full inspection completed on the home before purchasing it, you’ll need to pay for one privately and separately.

VA Minimum Property Requirements Homebuyers Should Know

The VA’s MPRs might seem lengthy to you at first glance, but they actually cover the basic safety, soundness, and sanitary features you should look for in a home. From the roof down to the crawlspace, the VA’s Minimum Property Requirements partly determine VA loan eligibility to ensure that your home is likely a sound investment.

When your loan officer orders a VA home loan appraisal, you can expect the home inspection portion to look for the following Minimum Property Requirements:

Property is Residential

The home you’re considering must be a residential property rather than a commercial property. However, the VA does allow you to purchase a home that is partially used for business, but only if the property is primarily residential. Similarly, your property must be zoned for residential use and conform to current zoning policies for your area. Your property can be a single-family, modular, or mobile home, and it must be your primary residence.

The reason for this VA requirement is that VA home loans are designed to assist veterans with their home purchase. Veterans can utilize other loans and grants geared toward veterans to help them fund a business and location.

Working Electricity

To meet VA approval MPR requirements, the home you’re considering needs to have safe and working electricity. The electric system in the home should be adequate to power necessary appliances and lighting. However, your appraiser is not required to turn on any appliances or lighting. Still, if wiring in an area of the home is known not to work or is deemed unsafe, you or the seller may need to repair it before the VA approves a loan.

No Exposed Wiring

Along similar lines, the VA won’t approve a home loan for a house that has exposed wiring or unsafe electrical system features. The house will need to fall in line with local building codes, too, which could mean that the VA requires test and reset buttons on all GFCI outlets or an upgraded circuit breaker from a fuse box. Frayed and visible wiring will need to be repaired no matter where your house is located.

Functional Heating and Cooling System

Your appraiser will look for adequate heating, especially in areas where plumbing exists. Your heating system must be able to maintain a temperature of at least 50 degrees in plumbing areas. The home’s cooling system must be in good working condition with no signs of unsafe or unsanitary features. The VA may also approve solar heating and cooling if the home has a backup heating and cooling system available.

Adequate Roofing

Most appraisers will consider the roof of a home one of its most important aspects. Any current or potential issues with a roof will likely be noted in an appraisal and a home inspection.

The VA considers the roof a crucial part of the VA MPR list. Specifically, your roof must not have any current leaks or problems that could lead to leaks, and it should have at least a few more reliable years of life left on it. The VA also requires the removal of old shingles if the home has at least three layers of old shingles that need repair.

Structure Is Free from Termites and Other Pests

There are two places in the VA’s Minimum Property Requirements in which termites and other damaging pests come into play for VA financing eligibility. The appraisal report will note any evidence of termites as a defective condition that affects the safety or sanitation of the property and in a section denoting wood-destroying insects, rot, or fungus.

Not all VA appraisals will require a wood-destroying inspection report. If an appraiser sees possible evidence of pests, the VA may require a separate inspection. Homes in areas with moderate to heavy termite infestation probability may also need a pest or termite inspection for VA approval.

Proper Water and Sanitation

Your home needs more than running water to get a VA loan approval. It must also have safe drinking water, hot water, and a continuous supply of running water available for toilets, sinks, baths and showers, and drinking. Your bathroom(s) must also be in a sanitary condition.

The VA also requires a safe method of sewage disposal. The appraiser may check to see if the home has an individual water supply and sewage system or that the utilities connect appropriately to your city’s water and sewage system.

Walls Free from Mold

Visible mold on walls, floors, or other areas of the home will be a significant concern for the VA when considering your home purchase loan. The appraiser will also check for leaks or potential water leaking into a home that could cause mold, including in your attic, basement, or crawlspace. Mold can rot the wood in a house, creating an unsafe structure, and it can be harmful to your health.

Proper Drainage and Free from Water Damage

Similarly, your home should have adequate drainage from gutters, downspouts, drain pipes, and other features of the home that help to move water away from its foundation. Pooling water in or around the house could result in a loan denial from the VA and VA lender.

Accessible Property Year-Round

Another VA MPR focuses on the accessibility of your property. The VA’s guidelines note that your property must have safe access for vehicles or people, like a driveway or sidewalk, from a road with an all-weather surface. In this case, a dirt road may not suffice. If your property has a backyard, you must also be able to access it without stepping on another property.

Free from Lead-Based Paint

Another VA loan requirement states that your property must not contain any lead-based paint. Paint no longer has lead because of the severe health risks it can impose, including memory loss, gastrointestinal problems, heart conditions, and kidney issues.

If the home you want to buy contains lead paint, the appraiser will note it in the appraisal report. The VA will require you to remove the paint and repaint the home unless it determines that the lead paint level is lower than the law-permitted level.

Sufficient Living Space

For VA home loan eligibility, your property must have sufficient living space, including places for sleeping, cooking, using the restroom, and living. The VA doesn’t specify a minimum area requirement for a home, but it does require that your home has adequate facilities and an area that’s suitable for safe living.

Accessible Attic and Crawlspace

A VA appraiser may not spend much time in an attic or crawlspace, but he or she does need to have access to it. Your attic and crawlspace should at least have a small access door for the appraiser to be able to take a quick look and snap some pictures. If the home doesn’t allow access to either space, the VA will likely require a fix before approving your mortgage.

What Are VA Minimum Property Requirements?

VA home purchase transactions can typically go smoothly when a home’s price matches its appraised value and the appraisal doesn’t note any serious conditions that go against the VA’s Minimum Property Requirements. Although snags in the process can happen when something needs to be prepared, try to remember that the MPRs the VA requires are designed to help you get the property to a safe, sanitary, and sound living standard.

You always have the option to walk away from a property if it requires more repairs than you or the seller are willing to deal with. Otherwise, a few fixes could help you purchase the home you love while benefiting from the many perks that come with a VA home loan.

Benefits.com is here to help you learn more about the options available to you.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.