The U.S. Department of Veterans Affairs provides several benefits to active-duty military members and veterans. In addition to disability compensation, veterans pensions, and paid training programs, the VA offers housing assistance in the form of VA home loans. To qualify for this type of loan, you’ll need a VA appraisal to assess the fair market value of the home you want to buy or refinance.

What Is a VA Appraisal?

VA appraisals can help a home buyer who is eligible for VA benefits to purchase a home with no down payment or private mortgage insurance and relaxed credit requirements. Although the appraisal process can seem intimidating, it helps protect both your purchase and the VA’s investment in guaranteeing your loan with your mortgage lender. With the guidance of the VA and your mortgage company, you can complete the VA appraisal and be one step closer to owning your home.

13 Common Questions About VA Appraisals

- What is a VA appraisal?

- Is a VA loan appraisal mandatory?

- How do I order a VA appraisal on a VA loan?

- Who pays for the appraisal?

- Can the buyer be present at the appraisal?

- What are the VA’s Minimum Property Requirements?

- How long does an appraisal take?

- How do I check the status of the appraisal?

- What is a Notice of Value?

- Can the seller see the appraisal?

- How long is a VA appraisal good for?

- What happens if a VA appraisal has complications?

- Can I dispute a VA appraisal?

If you’re considering using a VA loan to fund the purchase or refinancing of a home, you’ll first need to go through the VA appraisal process. Like a conventional loan, a VA loan requires an appraisal to determine if the asking price of the home is fair and that the house is safe and sanitary. These property requirements ensure that you, the home buyer, are purchasing the home for a reasonable price and interest rate.

Final acceptance of your VA loan hinges on the VA appraisal process. The VA will consider the appraised value and any notes the appraiser lists regarding the condition of the property before deciding whether to approve your VA home loan.

13 Common Questions About VA Appraisals

VA home loans offer several benefits to members of active duty and military veterans, including low closing costs and no required down payments. However, there are many steps the buyer must complete before getting approved for a loan, and the home appraisal is one of them. Here’s what you need to know about the VA appraisal process.

1. What is a VA appraisal?

For those who qualify for VA benefits, a VA home loan can be an excellent way to finance a housing purchase. A VA loan is like a traditional home loan, but it’s a form of VA financing for a home in which the VA guarantees its backing rather than a private lender. If a VA buyer defaults on the mortgage loan, the VA will be responsible for paying the loan debt to the private lender.

Before the VA issues a home loan, an approved VA appraiser must conduct an appraisal according to VA standards. The appraisal will determine the value of the home based on its condition and the prices of comparable homes. It will also note if the home is sanitary and in a safe condition for the home buyer.

2. Is a VA loan appraisal mandatory?

Yes. As part of the VA loan requirements for housing assistance, the VA does require VA borrowers to have a VA appraisal. The reason for this requirement is to ensure that the home is priced reasonably and that it’s in reasonable condition to protect both the buyer’s investment and the VA’s risk of guaranteeing the loan.

If you refuse to complete the VA appraisal process, then the VA has the right to refuse your loan. Similarly, hiring an appraiser that isn’t approved by the VA for your appraisal will result in a denied appraisal and loan.

3. How do I order a VA appraisal?

For a conventional loan, a loan officer typically orders the appraisal before approving the loan. The process is similar to a VA home loan, but the loan broker must order the appraisal through the VA portal. This is an online portal through which the mortgage lender can view your loan application and appraisal information.

Through the portal, the broker clicks the link for requesting a new appraisal and fills out all required sections to order the VA appraisal. Your broker should let you know when it’s the right time in the buying process to order the appraisal.

4. Can the buyer be present at the appraisal?

Yes. Nothing states that the VA buyer, seller, and even real estate agent, cannot be present at the time of the appraisal. However, the seller may want to be present or may not allow the buyer access to the property. Generally, appraisers won’t discuss their findings with you even if you are present, so being there may not help you find out anything sooner. Regardless of whether you’re present for the original appraisal, you’ll still get a full copy of the appraisal report when it’s ready.

5. Who pays for the appraisal on a VA loan?

The buyer will need to pay for VA appraisals. Because you’re the one applying for the loan, you are responsible for the cost of the appraisal. The VA appraisal fee can vary by location and the size of the property, but it usually costs between $500 to $800. You’ll need to pay this fee before the lender requests a VA home appraisal.

6. What are the VA’s Minimum Property Requirements?

Minimum Property Requirements are necessary points that a home will need to meet to be approved for a VA home loan. These requirements are similar to those for a USDA loan, FHA loan, and other government-backed loans.

MPRs are in place to ensure that you’re purchasing a safe and sanitary home, including things like adequate heating, a dry basement or crawlspace, and no lead-based paint. If any of the VA Minimum Property Requirements aren’t met as noted in the appraisal, the VA will likely deny your loan.

7. How long does an appraisal take?

The appraisal itself may only take about 30 to 60 minutes, depending on how large the property is and how in-depth the appraiser is. It usually takes seven to ten business days from the day your lender orders the appraisal to the day you receive the final report, although the time can vary depending on where you’re located. Your VA lender will notify you as soon as they receive the report.

8. How do I check the status of the appraisal?

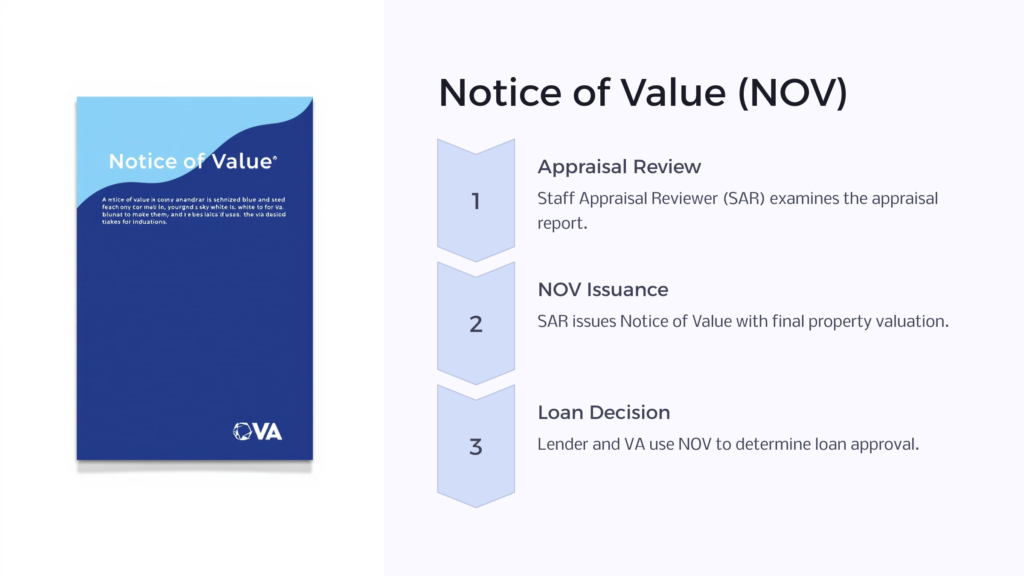

The only way to check the status of the VA appraisal process and the final report is to check with your lender. Your VA lender will receive a copy of the report – usually electronically – as soon as a Staff Appraisal Reviewer (SAR) has reviewed it. Your lender should let you know when the appraisal is ready for you to review and can send you a copy electronically, in person, or by mail.

If it has been more than 10 business days since the appraisal was ordered and you still haven’t heard anything, you can check with your lender.

9. What is a Notice of Value?

A Notice of Value comes from the SAR who reviewed the final appraisal report. The NOV will include the final appraisal value of your property’s value and will list the Minimum Property Requirements, if any, that the home failed to meet. The lender and the VA will use the NOV information rather than the initial appraisal to determine whether to approve your loan and the loan amount.

10. Can the seller see the appraisal?

You are under no obligation to allow the seller to see your final appraisal, NOV, or any information contained in them. The appraiser will only send a copy to your lender, who will then send a copy to you. You can then decide whether you want to share information from the home appraisal with the seller.

However, if there are any problems indicated in the VA appraisal, like a home value that’s much lower than the sales price or if the VA requires repairs before approving the mortgage, it could be in your best interest to share the report.

11. How long is a VA appraisal good for?

A VA appraisal is good for six months from the date of the appraisal. If other factors delay your mortgage loan process past the six-month expiration date, you’ll need to pay the appraisal fee again and have another appraisal completed.

After you close on your loan, the VA appraisal expires. This means that you cannot use the appraisal again for any other purpose that would require you to obtain a VA appraisal on your home.

12. What happens if a VA appraisal has complications?

Your VA home appraisal may not come back with the news you were hoping for. Sometimes, a VA appraiser may mark that the home value is lower than the selling price. In this case, you’ll either need to ask the seller to lower the purchase price or choose not to purchase the home.

An appraisal may also show repairs that will need to be fixed before the VA will approve your loan. Anything that doesn’t meet MPRs will need to be fixed. You can ask the seller to repair the issues, but if the seller refuses, you’ll be responsible for the repairs if you want to continue pursuing your loan.

13. Can I dispute a VA appraisal?

Although you cannot get a new VA appraisal if the first one didn’t meet your expectations, you can ask for an appeal, also known as a Reconsideration of Value. During this process, those involved in the ROV process can review any information you, the seller, or the lender present, including other comparable homes in the area that the appraiser didn’t consider and your reasoning for requesting the appeal. The ROV won’t guarantee a changed outcome or an appraisal update, but it also can’t hurt.

VA Appraisal vs Home Inspection

It’s important to understand that a home inspection is different from a VA appraisal. While a VA home appraisal focuses primarily on a home’s value, the home inspection provides a more in-depth look at any current or potential issues with the house. A VA appraisal will check the basics, like the safety of your heating and electrical systems and the condition of the roof. However, it won’t include an HVAC, water damage, termite inspection, or other more comprehensive inspections of the home.

A VA appraisal will be a relatively quick visit compared to a home inspection. You can expect your appraiser to visit the home for up to an hour, but it could take up to four hours or more for an inspector to complete your inspection.

For more advice on the application process, Benefits.com is here to help. We offer front-end support for gathering medical evidence and have advised thousands of veterans on how to get the benefits they medically, ethically, and legally deserve.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.