When it comes to automobile ownership, most states require drivers to carry car insurance. Unfortunately, the same is not true for life itself. But while the benefits of having life insurance as a hedge against misfortune are clear, you might be surprised to learn that life insurance also provides some retirement planning benefits.

5 Ways Life Insurance Can Help During Retirement

- Helps you reach your savings goals

- Helps protect your income

- Improves portfolio returns

- Provides peace of mind

- Helps manage taxes

The basic premise of life insurance, like any insurance, is simple. Individuals can subscribe to an insurance policy by paying a periodic premium. Most life insurance companies will establish the value of this premium after an actuary has assessed the applicant’s health and likelihood of mortality. In some cases, they may decline to cover an individual, but most people can secure life insurance, especially if they are younger and healthy.

If the subscriber dies, the life insurance company will pay out a death benefit to the beneficiaries listed in their plan, which in most cases is their immediate family (spouse and children). Ideally, these death benefits are used to defray the cost of a funeral and provide a source of income for the family or surviving spouse until they are able to rebuild an income stream on their own. In some cases, especially when a spouse is already older, they may continue to rely on this income stream for the rest of their life.

But life insurance is not just about protecting a family’s cash flow in the event of a breadwinner’s death. In many cases, there are added levels of investing and tax-sheltering complexity that can make a life insurance policy an attractive place to save and grow money with an eye towards retirement. In general, the protective premise of a life insurance policy can make it easier to protect vulnerable streams of retirement income from untoward loss—for instance, when a retiree loses their retired spouse and is no longer able to work.

What is a Life Insurance Retirement Plan (LIRP)?

A life insurance retirement plan combines the benefits of a retirement fund with life insurance coverage. A LIRP is a life insurance policy where subscribers pay above and beyond the required premium so that they can borrow against the accumulating cash value by taking out a tax free loan during their retirement. You might wonder why a LIRP should be part of a retirement strategy, especially for individuals who already have a retirement account funded by decades of dedicated retirement saving contributions. Why would they need a loan?

The answer lies in the fact that periodic withdrawals from a traditional IRA and even a Roth IRA—where earnings can grow tax free—are considered taxable income. When added to the Social Security a retiree or retired couple filing jointly collects, this can result in a sizable chunk of cash with no tax advantage, and it can even increase the tax penalty on Social Security income, specifically. By contrast, taking out a policy loan, as it’s called, against the accumulated cash of your LIRP is not considered taxable income (it’s a loan, after all), and as a result, it can yield some serious tax savings.

This strategy afforded by life insurance retirement plans won’t be necessary for everyone. But a policy loan can be a great tool for avoiding or minimizing income tax during retirement, so it’s certainly worth talking to a financial professional and seeing if a life insurance retirement plan should be in your financial future.

What Are the Main Types of Life Insurance?

There are two main categories of life insurance coverage: protection policies and investment policies. A term life insurance policy generally offers a lump sum payment to a beneficiary or beneficiaries in the event of the policyholder’s death as long as it occurred during the term of coverage. The premiums that they pay on a monthly basis for this term life insurance policy do not accrue any kind of cash value.

Investment policies, on the other hand, are a form of cash value life insurance that offer an investment option in addition to their inherent life insurance benefit. Whole life, universal life, and variable life are examples of a permanent life insurance policy where the contributions are accumulated as capital from which the policyholder can withdraw money, borrow money, or surrender the policy and obtain its surrender value.

Term life insurance is typically the most cost effective way to purchase life insurance, as the premiums tend to be lower. This type of life insurance plan has a fixed term, the expiration of which means that the subscriber will have to renew their coverage or seek coverage elsewhere—but either way, they are not guaranteed the same rates they had in the now-expired term.

Whole life insurance is an insurance policy that offers protection for the subscriber’s entire life, as long as they pay their premiums in full for as long as they need to. Incidentally, they may only need to pay their premiums up to a certain age to fulfill their end of the contract and obtain coverage for the remainder of their life. In addition to the death benefit offered by such a permanent life insurance policy, the contributions made beyond the premium can snowball into a serious amount of capital that affords options for withdrawals, loans, and payouts upon its complete maturation.

Universal life insurance is similar to whole life insurance in that it covers the subscriber their entire life, but it offers more flexibility in terms of adjusting the premiums and death benefits if you’ve accumulated enough money toward the policy and you pass a medical examination. Universal life insurance policies can also function as a sort of savings account; dollar amounts contributed in excess of the policy premium can increase based on current market rates or the minimum interest rate.

Variable life insurance is similar to a mutual fund in that the death protection benefit can be invested in stocks, bonds, and other types of tradable equities. As such, this cash value account can increase, but it also runs the risk of decreasing. However, some variable life insurance policies guarantee that the value will not fall below a certain threshold.

These are the different types of life insurance. As you can see, term life insurance is useful for safeguarding against unfortunate circumstances, but the cash you put into the life insurance coverage can never be reclaimed. By contrast, the other types of life insurance policies—whole life insurance, universal life insurance, and variable life insurance—can provide an investment vehicle in addition to their function as life insurance. As such, they can become useful tools for a retirement strategy.

5 Ways Life Insurance Can Help During Retirement

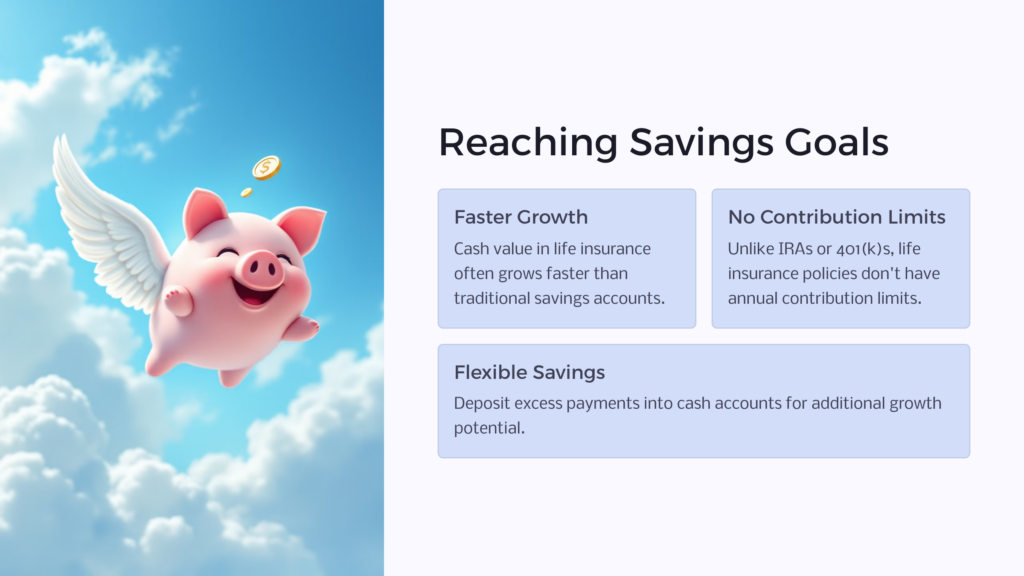

1. Helps you reach your savings goals

Some types of life insurance like Universal life insurance allow you to deposit payments in excess of the premium toward a cash account that can grow in value. This can be a convenient way to quickly reach your savings goals since the rate at which your life insurance policy grows will often be much faster than a traditional savings account or CD. It’s also important to note that a Roth IRA, 401k, and traditional IRA will often have annual contribution limits (usually $6,000 per year per account and $7,000 for those 50 and older). By contrast, life insurance retirement policies do not have contribution limits, so it can be easier to reach your savings goals.

2. Helps protect your income

If you are already in retirement, still married, and both spouses are collecting a Social Security check or some other form of income, you will want to protect that income stream. If one of the spouses passes, the income could be cut in half. A life insurance policy will protect the income stream and prevent it from being reduced for the surviving spouse in the event of the other’s demise.

Surprise medical expenses can also wreak havoc on retirement income. With people living longer than ever before, it’s more than possible that retirees will face surprise medical expenses. If one spouse’s income has been removed from the equation, that can become a particularly burdensome quandary.

3. Improves portfolio returns

Different types of investments have differing amounts of volatility. In the main, stocks express a higher degree of volatility than government bonds. Some investment portfolios are weighted down by a percentage of bonds, the relative stability of which can offset any losses from the vacillating prices of stocks.

Bonds have risk as well. If interest rates rise, the price of bonds can go down, which negatively impacts their return on investment. That’s why some investors use a life insurance policy instead of bonds in their retirement portfolio. Many life insurance policies have a return that is similar to bonds, but without the same vulnerability to rising interest rates, making them an attractive substitute.

4. Provides peace of mind

In the years leading up to retirement, both spouses are most likely actively working to make those few final pushes toward the nest egg they’ve been hoping for. If one of the spouses passes, that can leave the surviving spouse struggling to catch up and save enough money for retirement—especially if there have been unexpected expenses like medical treatments, in-home care, or a funeral.

Life insurance can help provide peace of mind around entering retirement so that both spouses know that not even death can derail their financial goals. Some permanent life insurance plans will even offer an advanced payout in the event of a terminal illness that necessitates intensive care, so these policies can provide peace of mind with their function as long term care insurance.

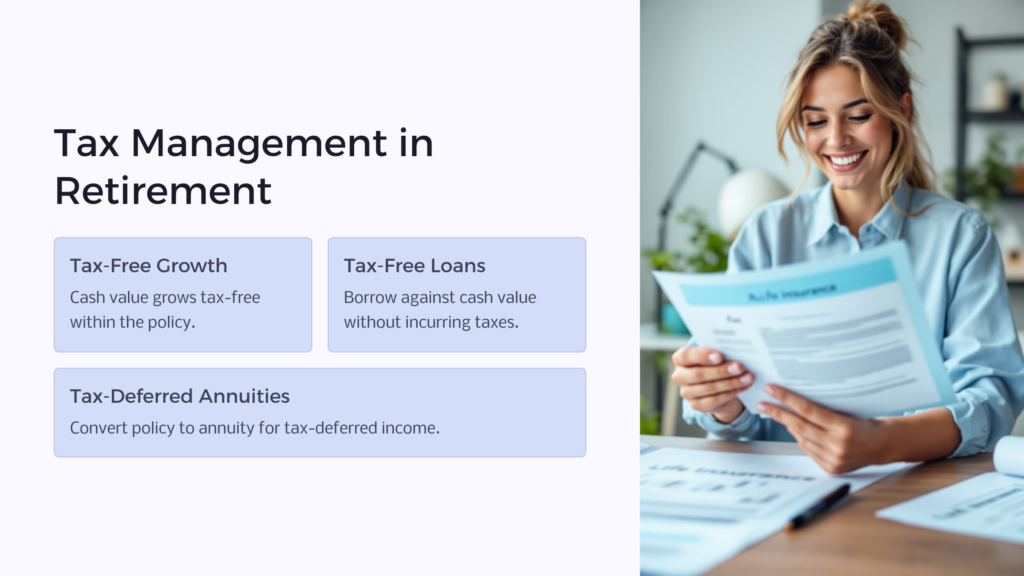

5. Helps manage taxes

Life insurance policies with cash value get preferential tax treatment. They can provide a tax free shelter for growing your money, and even obtaining tax-free cash flow and tax-free death benefits, when properly structured. One way that a life insurance policy can provide cash flow with preferential tax treatment is through annuities.

Some policies will allow the subscriber to stop paying premiums after a certain point and instead collect a periodic payout from the insurance company: an annuity. These annuity payments are not tax free, but they are tax-deferred. However, annuities funded with a Roth IRA or 401K can sometimes be tax free if certain conditions are met. Also keep in mind what was said at the outset of our article, that a policy loan can be taken out against the cash value of the LIRP, and loans are not considered taxable income.

Consider a Life Insurance Retirement Plan

Life insurance is traditionally thought of as a way to defray the costs associated with death (such as a funeral) and provide an income for surviving family members. While all this is true, life insurance also has some monetary benefits in terms of retirement planning, so much so that it might as well be considered retirement insurance.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.