Being able to claim your Social Security retirement benefits is a huge milestone for any American worker. Before you apply to receive your monthly benefits, there are a few key facts you should know about what to expect when it comes to your Social Security check. We’ll walk you through everything you need to be aware of so that there are no surprises when you receive your first monthly benefits.

7 Common Questions About Your Social Security Check

- What is a Social Security check?

- When are Social Security checks paid?

- Are Social Security checks still mailed?

- How do I set up direct deposit?

- What is the average Social Security check?

- Why is my Social Check less than expected?

- Do I need to pay taxes on my Social Security Check?

Your Social Security retirement benefits can be an important component of your overall retirement income, so it literally pays to know as much as you can about what to expect when it comes to receiving your monthly benefits check. If you’re unsure about the details of your Social Security check, keep reading – we’ve outlined all the important facts associated with how the Social Security Administration will deliver your benefits.

What Is a Social Security Check?

Your Social Security check represents the monthly amount the Social Security Administration has determined that you’re eligible to receive, based on the number of years you’ve worked and the number of Social Security work credits you’ve accumulated.

When to begin receiving your Social security benefits is up to you, to a large extent. You typically can’t begin receiving them before 62, and you won’t get your full monthly benefit until your full retirement age, which for most people is age 67. If you can defer your retirement benefits until age 70, you’ll receive the highest possible monthly benefits amount. Once you know when you’ll want to start receiving your benefits, all you have to do is apply for them online. Keep in mind that Social Security retirement benefits aren’t meant to fully replace your working income. Making sure you have other sources of retirement income and that you can wait as long as possible to begin collecting your benefits can help you make the most of your benefits.

It’s also important to note that Social Security benefits are paid to other recipients besides retirees – although retirees compose roughly 76% of benefits recipients. The SSA also pays Social Security benefits to those with disabilities who can’t work, and to survivors who draw benefits based on someone else’s work history. Disability recipients represent approximately 15% of Social Security benefit recipients, while survivors make up the remaining 9%.

When Are Social Security Checks Paid?

Your Social Security check date depends on your birth date. You could receive your payment on the second, third, or fourth Wednesday of the month, depending on the day you were born. If you were born the first through the 10th of the month, you’ll receive your check on the second Wednesday of the month. Born from the 11th through the 20th? Expect your check on the third Wednesday of the month. And those born between the 21st and the last day of the month should expect their Social Security payment on the fourth Wednesday of the month.

Understanding the timing of your Social Security retirement benefits can help you plan how to use your retirement income. It’s also important to note that Social Security benefits are paid for the previous month – so the check you receive in August is for July’s benefits, etc.

Of course, there are some exceptions to this schedule, including those who are receiving benefits based on someone else’s work record, those who began receiving benefits before May 1997, and those who receive both Social Security retirement benefits and Supplemental Security Income benefits. And if your payment day falls on a holiday, you’ll likely see your funds appear the day before your scheduled payment.

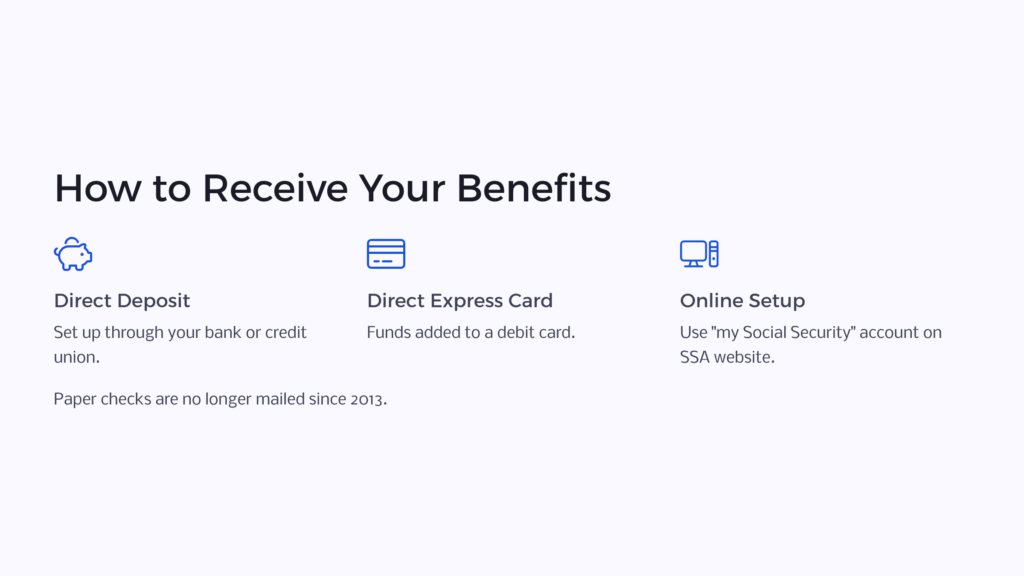

Are Social Security Checks Still Mailed?

Actually, no. Since 2013, the Social Security Administration no longer mails paper Social Security checks, so to receive your benefits, you must set up direct deposit through your bank account. You can also have your benefits deposited on a Direct Express debit card, which you can then use to make purchases and pay bills.

How Do I Set Up Direct Deposit?

You can usually set up direct deposit through your bank or credit union. It’s generally as simple as providing the routing and bank account numbers so the SSA can electronically deposit your funds. If you have already set up a “my Social Security” account through the SSA website, you can log in and supply the necessary information to have your funds deposited. If you don’t have a My Social Security account, you can also call the SSA and/or visit your local SSA field office to make the necessary arrangements to receive your funds electronically.

Your other option is to have your Social Security benefits added to a Direct Express debit card. Your funds would be added to your card the same day they’d normally be deposited into your bank account. You can then use your Direct Express card just like you would a bank debit card – to pay for purchases in stores, to pay bills, etc. You’ll need to make sure you understand the terms from your specific bank, though – there may be fees associated with some Direct Express card transactions.

What Is the Average Social Security Check?

According to the Social Security Administration, the average Social Security monthly retirement benefit is $1,390.12. But it’s important to note that this includes anyone who receives any type of monthly Social Security benefit, not just retirees. These groups may include those who receive Social Security disability benefits, those who receive spousal benefits, or those who receive Social Security survivors’ benefits. For the average retiree, that average amount increases to $1,512.63.

The maximum amount you can receive in Social Security retirement benefits depends on a few factors: your age at retirement, your earnings over your working life, and your incremental cost of living increases. For 2020, for example, the maximum benefit for someone who retired at age 62 would be $2,265, and the maximum for someone who waited until age 70, when required to draw benefits, would be $3,790.

Why is My Social Check Less Than Expected?

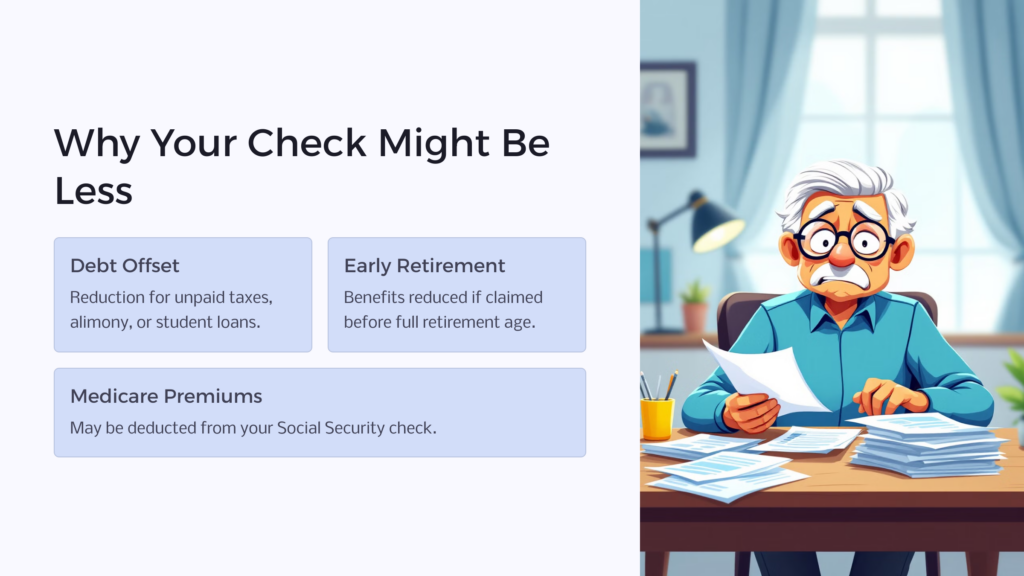

If you have just started drawing your Social Security retirement benefits, you may be surprised to find that your monthly checks are less than you expected. This could be for several reasons, including any of the following:

- You owe certain debts, like back taxes, unpaid alimony or child support, or student loans. This is called an offset for debt, and the SSA will reduce your benefits by a set amount until the debt you owe is paid. The SSA, however, will protect the first $750 of your benefits check.

- Your income from working after retirement is more than you expected, which may require you to pay income tax on your benefits.

- You began taking Social Security retirement benefits early, which keeps you from being able to draw the full benefit amount. In some cases, taking early retirement benefits can reduce your monthly payment by as much as 30%.

- Medicare premiums may have reduced your benefit amount. This can happen if your total retirement income ends up putting you in a higher tax bracket than you expected. For some people, Medicare premiums may cost them 30% to 80% of the total cost of coverage.

This is why it’s so important to work with a trusted financial advisor before you retire to make sure you don’t have any outstanding debts and that you fully understand your retirement income amount and how it affects everything from Medicare premiums to income taxes. Making a wise choice about when to begin collecting your Social Security retirement benefits also is crucial. You don’t want to be surprised by monthly checks that are smaller than you expected.

On the opposite end of the spectrum, from time to time, you may notice changes in the amount of your Social Security retirement benefits that work in your favor. Usually, this means an increase in your benefits amount – the SSA will adjust the amount of your check at least once per year to cover inflation. This cost of living adjustment typically is calculated in October and begins being paid out in January. This adjustment is typically pretty small; in fact, for 2020, it was a 1.6% increase.

Do I Need to Pay Taxes on My Social Security Check?

You might. It all depends on your financial situation, and especially whether you’re receiving any other retirement income – for example, if you continue working after retirement in a reduced capacity. This can also happen if you have significant assets from which you continue to draw income throughout your retirement.

Before you retire, you can sit down with a Social Security benefits advisor and look at your estimated retirement income. This can also help you determine when is the best time to begin drawing your Social Security retirement benefits in order to keep your taxes as low as possible throughout your retirement. If you think you might be in a situation where you make enough money to render your Social Security retirement benefits taxable, you can always request for income tax to be withheld from your benefits when you sign up, at a rate of 7%, 10%, 12%, or 22% percent. You also can make estimated quarterly tax payments to the IRS.

Understanding Your Social Security Check

According to the Social Security Administration, approximately 45 million retired American workers receive Social Security retirement benefits each month – your Social Security benefits are an important part of your retirement income, so it’s important to understand how your benefits are calculated and what you should expect from your monthly check. It’s also important to keep in mind that Social Security retirement benefits never were envisioned as composing the entirety of a retired worker’s income.

While Social Security benefits are an important retirement income supplement, you should work with your financial advisor to determine what kind of retirement savings plan – ideally through your employer, with an employer match – can help you reach your retirement goals. Between your savings and the supplemental income you receive through your Social Security retirement benefits, you can shape the retirement income that allows you to lead a fulfilling post-retirement life.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.