Bankruptcy can force potential homeowners to change their plans, but it doesn’t always have to—especially for veterans and active duty personnel.

4 Tips About VA Home Loans and Bankruptcy

- How to Qualify After a Chapter 13 Bankruptcy

- How to Qualify After a Chapter 7 Bankruptcy

- Ways to Improve Your Credit Score

- How to Qualify After a Foreclosure

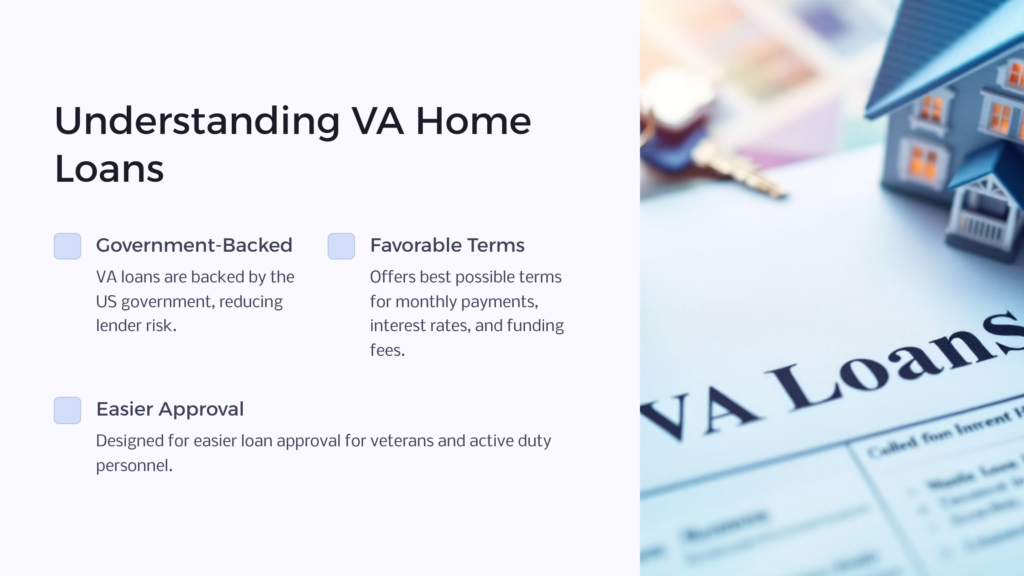

VA financing in terms of a mortgage loan is administered by the Department of Veteran’s Affairs, but the mortgage loan itself comes from a private mortgage lender or an institutional bank. However, a VA mortgage differs from a conventional loan in several ways. Unlike a conventional loan, a VA mortgage is backed by the US government. If the VA borrower defaults on the loan, the government will compensate the mortgage lender for part of the loan amount. This means that a lender or loan servicer faces less risk in extending a home loan to a VA buyer. They can provide veterans and service members with the best possible terms regarding monthly mortgage payment amounts, the interest rate, and the funding fee.

VA home loans are similar to USDA loans and FHA loans, though the latter two are geared towards home buyers of limited financial means. And while VA loans are not specifically intended to provide housing for a borrower with less income, they are intended to provide easier loan approval for military veterans and active duty personnel in return for the services rendered for their country.

What is Bankruptcy?

Bankruptcy is a legal process one can go through to seek relief from debts they cannot repay. Though these debts come from any number of sources, the most common acute incidents and ongoing crises that can cause bankruptcy are medical expenses, layoff, poor use of credit, and divorce or separation.

There are different kinds of bankruptcy, but after the bankruptcy process has been completed, the person(s) who filed for bankruptcy will have their debts discharged, with some exceptions such as debts for loans obtained under false pretenses or from taxes, student loans, alimony, and child support.

However, credit card debts, home loans, and auto loans are a few debt types that will be wiped away, unless an individual should choose to reaffirm some of their debt—something that unscrupulous creditors may try to trick the filer into doing. In some types of bankruptcy, a bankruptcy trustee will help the filer work out a payment plan so they can retain their assets. After its completion, the remaining debt will be forgiven or discharged.

Once these debts have been discharged, the individual who filed for bankruptcy can begin to repair their finances and their credit score. It takes about 1-3 years before an individual who has filed for bankruptcy will qualify for a larger type of debt like a home loan. Until then, a credit report from any credit bureau will show the bankruptcy filing in their recent history, and they may not have yet indicated to potential lenders that they have the financial solvency to take on the burden of a monthly payment for a home.

Can I Get a VA Home Loan After Bankruptcy?

Anyone can get a home loan after bankruptcy, providing they have improved their credit history, improved their spending habits, and can exhibit financial solvency. It generally takes anywhere between one to three years before an institutional lender like a bank would be comfortable giving such a person a large loan like a mortgage. But the good news is that it’s even easier for a veteran or active duty service member to secure home financing after bankruptcy since the bounce-back time for a VA loan is shorter.

Securing a VA home loan after undergoing foreclosure requires a waiting period of three years, while a Chapter 7 bankruptcy requires a waiting period of two years. A Chapter 13 bankruptcy where the filer exhibits a 12-month history of on-time payments can have a waiting period as short as one year. Some VA lenders may have more flexible requirements, but these are the general wait times. It is possible to secure a VA home loan after bankruptcy, but not right away.

4 Tips About VA Home Loans and Bankruptcy

VA loans come with many perks, including the ability to buy a home with no down payment, which is normally a significant hurdle for most home buyers. But some veterans or active duty service members with a bankruptcy filing in their financial history may be worried about their VA loan eligibility.

1. How to Qualify After a Chapter 13 Bankruptcy

Chapter 13 Bankruptcy is often referred to as “reorganization bankruptcy” because it does not involve wiping away your debts, but rather creating a structured payment plan to pay them down. If you have gone through 12 monthly on-time payments toward paying down your debt, you may be able to find a VA lender who will extend a home loan, provided the judge or trustee overseeing your Chapter 13 bankruptcy approves. It goes without saying that if you’ve completed the payment plan and resolved your debts, you can secure a VA loan—but the lender will still want to see that you meet financial and income-based standards.

2. How to Qualify After a Chapter 7 Bankruptcy

Chapter 7 Bankruptcy is often referred to as “liquidation bankruptcy.” Your debts (with some exceptions) will be discharged—but first, any items of value in your possession may be seized and sold to pay off the debts. If an individual does not have any items of significant value, such as a vehicle, home, jewelry, or cash above a certain dollar threshold (which varies by state), then they won’t need to liquidate assets to satisfy their debt.

In any case, after two years of having your debts discharged, the Department of Veterans Affairs will disregard it when you apply for a VA loan. If your debt was discharged between one and two years, you may still qualify if you can exhibit an improved credit history and prove that the bankruptcy was caused by circumstances beyond your control.

3. Ways to Improve Your Credit Score

The first step towards improving your credit score is improving your financial life. This involves learning how to budget and avoid spending beyond your means. For most individuals, this will go a long way towards preventing future bankruptcy, and it will also improve their credit score—a ranking system used by banks and lenders to determine a potential borrower’s sense of trustworthiness in regards to repayment. Bad credit indicates there is a risk in lending someone money, while good credit indicates the opposite.

Using cash instead of credit cards, not spending more than 33% of your income on housing, shopping wisely, and avoiding unnecessary expenses such as lavish vacations or expensive vehicles can go a long way towards improving your credit score.

You will need to establish some credit. One popular strategy involves taking out a secured credit card or one with a small credit line, using it for a small recurring bill every month, and making timely, in-full payments on it to rebuild your credit score.

4. How to Qualify After a Foreclosure

Like bankruptcy, a foreclosure on a previous residence does not preclude you from getting a VA home loan, but it typically requires a two-year waiting period. However, if the foreclosure property was purchased with a VA loan, you may have reduced VA loan entitlement, which limits the amount that can be borrowed.

In addition to the wait time, you may need to secure and provide a borrower’s Certificate of Eligibility that indicates how much entitlement you possess in terms of securing a favorable VA loan. This Certificate of Eligibility, also referred to as COE, is the standard form used by veterans and active duty service members to confirm their eligibility for a VA loan, in terms of their service and financial history with previous VA loans.

What’s the Difference Between Chapter 7 and Chapter 13 Bankruptcy?

Chapter 7 Bankruptcy is generally meant for people with limited financial means who will not be able to pay back their debts, or even part of their debts. Personal property that isn’t exempt from being sold will be liquidated to compensate the creditors.

Laws vary from state to state, but most filers are allowed to retain up to $23,000 in homestead equity, a motor vehicle of up to $3,800 in value, and personal property up to $12,000, with a total exemption for healthcare equipment. As you might have guessed, $23,000 in home equity is less than a home for most individuals, so it most likely means giving up your home.

For that reason, some individuals who want to retain their assets will file for a different type of bankruptcy, Chapter 13, which involves a court-ordered repayment plan to compensate creditors for a portion of the debt owed them. After that portion is paid off, the remaining debt will be discharged. Chapter 13 bankruptcy is best suited for individuals who have the financial means to reorganize their finances and pay down a portion of their debt, as long as it does not exceed certain limits.

The process for Chapter 7 bankruptcy generally lasts 3-5 months, while the process for Chapter 13 bankruptcy usually lasts 3-5 years. Again, Chapter 7 bankruptcy is best for individuals who either have few possessions, pay rent instead of own, or have limited financial means. Chapter 13 is best for individuals who have some financial means and want to retain their property.

In regards to obtaining a VA loan after bankruptcy, a Chapter 7 bankruptcy ends with a clean slate, but it will be around two years before one can secure another VA loan. A Chapter 13 bankruptcy can see the filer obtaining a VA loan after just 12 months of on-time payments, if the overseeing trustee or judge approves.

VA Home Loan Bankruptcy

Veterans and active duty servicemembers benefit from VA loans, which make home buying easier for individuals who have sacrificed so much for their country. Zero down payment, lower closing costs, no prepayment penalty, easier qualifications, no loan limits, and no limits on the number of VA loans obtained are just a few of the benefits of a VA loan.

For individuals who have a bankruptcy in their financial record, obtaining a VA loan might become more difficult in the immediate aftermath of the bankruptcy. After a few years, it will be a much less important consideration for many lenders—especially for potential borrowers who have rebuilt their credit and exhibited good financial habits since their bankruptcy discharge.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.