What SSI is and Whom It’s Designed to Help

Supplemental Security Income (SSI) pays benefits to aged, blind or disabled persons with low income and modest resources who need financial assistance.

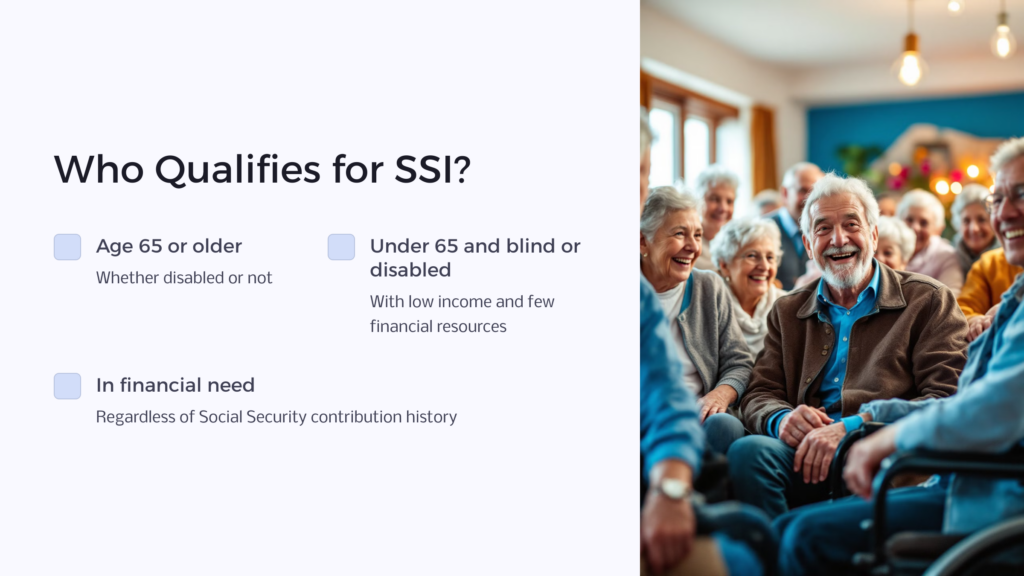

Supplementary Security Income is designed to help YOU, if you are…

- Age 65 or older (whether disabled or not) OR

- Under age 65 and blind or disabled AND

- you have a low income and few financial resources and are in financial need.

If you fit this description, SSI may be able to provide regular cash payments to help you meet your basic needs for food, clothing, and shelter—even if you have not paid into the Social Security system.

SSI is a federal income supplement (welfare) program funded by general tax revenues not by FICA payroll deductions (aka Social Security taxes). However, since they are uniquely set up for it, the Social Security Administration (SSA) handles all SSI procedures: the application process, determining who is eligible and who is not; appeals if denials are contested; payment authorization, and reduction or discontinuation of payments to those no longer fully eligible, etc.

No matter where you live in the USA, there is probably an SSA facility not far from you. With national headquarters in Baltimore, MD and nearly 60,000 employees, SSA has 1,230 local field offices, plus ten regional offices, six processing centers, 164 hearing offices, five National Hearing Centers, an Appeals Council, and numerous telephone service centers that can be accessed via a national toll-free number, 1-800-772-1213.

As of September 2016, there were approximately 8,287,000 SSI recipients (out of a total U.S. population of about 318.9 million). The number increased during the recent “Great Recession,” no doubt due to massive unemployment and less reluctance to apply for aid. So, if you’re eligible and need SSI assistance but have been embarrassed to apply, don’t be. If you’re like most recipients, your lack of sufficient income or resources was caused by conditions beyond your control.

But before you apply for SSI, please read this report and other articles you’ll find about SSI on this website. They can save you time by helping you avoid common errors or omissions, and by alerting you to the documents required to prove your eligibility.

How Supplemental Security Income Differs from Social Security Disability Insurance (SSDI) and How It’s Similar

Since both SSI and SSDI are administered by the Social Security Administration and have similar initials, confusion often occurs. However, the programs are quite different.

As noted, SSI is funded by general tax revenues of the United States—and, in most states, by additional state funds—while SSDI is funded entirely by FICA (Social Security) taxes and the money earned by the Social Security Trust Fund when the tax money is invested.

As also noted, SSI pays benefits based on financial need as defined by SSI law. SSDI, on the other hand, pays benefits only to persons who have worked and paid enough taxes to become insured or to an insured worker’s disabled adult child or disabled surviving spouse or disabled surviving divorced spouse of an insured worker regardless of their current income or financial resources.

What SSI Provides—How Much and How Often

SSI benefits are paid at different rates depending on several variables. For 2020, the basic monthly federal amount is $783 for an eligible individual and $1,175 for an eligible couple residing together ($578.50 each). The average monthly federal payment per person was about $551.37 in October 2018. At times, there is an automatic cost-of-living adjustment (COLA). In 2020 there is an increase of 1.6% based on a 1.6% increase in inflation from the third calendar quarter in 2018 to the third calendar quarter in 2019. In addition, most states supplement federal SSI payments with optional SSI state supplements, which vary by state and which are determined in part by your living arrangements, such as living independently or in a nursing home.

If you qualify for SSI benefits, you will receive monthly payments from the Treasury Department, sent electronically to your personal account at a bank, savings & loan, credit union or other financial institution. It can be a checking or savings account, or a money market account. SSI payments can also be made via the Direct Express Debit MasterCard program, which may be more convenient if you travel frequently, are not near a financial institution, or wish to keep the payments as confidential as possible. However, a debit card may not have the same financial protection as a bank account or credit card in regard to loss, theft or misuse.

Once you are eligible for SSI payments, you will receive them on the 1st of each month. If the first falls on a weekend or holiday, payments are made the preceding workday.

SSA strongly recommends an individual—not a joint—account. That’s because with a joint account, anyone named on the account can use the funds for themselves instead of for their intended purpose—your food, clothing and shelter. Additionally, SSA considers all the money in your joint account to be yours, even if it isn’t because once any money is deposited, you have legal access to it. Of course, this adds to the amount of your financial resources and if the total exceeds SSI limits, you can be denied SSI benefits. Additionally, the joint owner’s deposits may be counted as income to you.

How Your Financial Situation Helps Determine Eligibility for SSI

To help conserve available funds and pay benefits to the most needy, the SSI program has set limits to the amount of financial resources each recipient can have. Resources are anything you own, although not all resources are countable. In 2019, the resource limits are $2,000 for each adult or child, or $3,000 for each married couple. States that supplement SSI payments may have different limits. To find out what they are in your state, call your local SSA office. Some resources that count are cash, accounts in financial institutions, stocks, bonds, property that you do not live on and that is not income-producing property, usually a second vehicle, and money or items you loaned to others but fully expect to get back. (The repayments will not count as income.)

Similarly, limits are placed on the amount of income you (and your spouse if you are married living with your spouse) can have. If you are applying for a child, then income of the child’s parents and stepparents living in the same household is considered. According to terms of the program, income is money you receive and usually direct payment of your shelter and/or food costs. Examples are wages, self-employment earnings, tips, spare-time income, Social Security benefits, workers’ compensation, unemployment benefits, military pay and allowances, VA benefits, state disability payments, railroad retirement benefits, civil service benefits and pensions. It also includes certain royalties, honoraria, interest income, sheltered workshop payments, food, shelter, disaster relief funds, some other insurance payments to you, inheritance of cash or property or life insurance proceeds, annuity payments, dividends, rental or lease income, strike pay or other union benefits, settlements, alimony, child support, etc

Most people don’t realize that income also includes money from friends or relatives, gifts, lottery or sweepstakes winnings, gambling profits and other prizes.

Some types of income that SSA does not count include the following:

- The first $20 each month of most of your income.

- The first $65 each month you earn from working.

- Half the amount each month over $65 you earn from working.

- The value of any food stamps you receive.

- The value of shelter you get from some private nonprofit organizations or government subsidized housing.

- Most home energy assistance.

- Money you borrow with a bona fide loan repayment agreement.

- Some scholarships or grants, if you are an eligible student.

- Wages you use to pay for items (e.g., a wheelchair) or services that help you to do your work, if you are disabled but working.

- Any wages you use for work expenses (e.g., transportation to/from work) if you are blind and working.

- Infrequent and irregular income in low amounts.

Not counted as resources are the following:

- The home you live in, the land it’s on and related buildings.

- Normal household and personal effects.

- One wedding ring and one engagement ring, regardless of value.

- Necessary health aids; e.g., wheelchair or prosthetic device.

- Some grants and scholarships.

- Irrevocable life insurance policies with a face value of $1,500 or less.

- Social Security or SSI back pay for up to nine months. (Nine months after receipt, it counts).

- Your car (usually), regardless of value; the equity value of additional vehicles may be counted unless the second vehicle is needed for self-support.

- Other non-business property, up to a reasonable value, needed for financial self-support.

- Burial plots for you and for family members.

When applying for SSI benefits, it is very important that you list all your income whether or not you think it is excluded as well as all your assets so that Social Security can check to see if the totals of countable income and assets are less than the SSI allowable limits. Keep in mind that it may be difficult for you to assess financial eligibility yourself; therefore, unless you have liquid assets that are clearly over the limit, you should always file a claim to get a financial assessment.

How you might qualify for SSI even if you don’t right now

There are a few ways you might be able to legally reduce your income and/or assets in order to qualify for SSI benefits. With regard to income, if you are disabled and working, remember to claim all impairment-related work expenses.

To reduce your total resources (including cash) to less than the limit of $2,000 per person or $3,000 per couple—you can sell things. However, if you give away a resource or sell it for less than it’s worth or give away property or money just to become eligible for SSI, you will be ineligible for SSI, possibly up to 36 months after the gift or sale. If you sell a resource for what it’s actually worth, be sure to keep records of the sale and any documentation that it was sold for market value. Any money from the sale will count toward the resource limit beginning the first of the month following the month of sale.

You can, of course, use the proceeds from the sale or use other funds to pay ongoing normal living expenses or to purchase or pay on excluded resources such as buying a better vehicle or repairing your home or paying down the mortgage. You can also off debts or take care of deferred needs such as new tires or dental work or eyeglasses. You might also set aside money in a separate fund for our burial expenses or purchase an irrevocable life insurance policy with a value of up to $1,500. You and your spouse can set aside up to $1,500 each to pay for your burial expenses and it won’t count as a resource. This is in addition to excluded burial sites. However, if you also own whole life insurance policies that have cash value, the cash value will count toward the resource limit of $2,000 per individual or $3,000 for a couple and toward the $1,500 burial-fund limit.

Within a very narrow set of laws and rules, money can be transferred into a trust. A trust is a legal arrangement in which one party holds property for the benefit of another. A trust can hold cash, stocks or other liquid assets, and/or real estate or personal property that could, at a later date, be turned into cash. There are many kinds of trusts. SSA comments: “In some cases, we consider putting resources into a trust as a transfer of resources that makes you ineligible for SSI. In other cases, we count the trust itself as a resource. Moreover, the value of the trust could put you over the resource limit.” However, “We will not count the trust if counting it causes you undue hardship.” (Note that what defines undue hardship is not clearly defined.) But, they add, “Some trusts and trust payments that we do not count as your resources or income for SSI purposes can affect your Medicaid eligibility.” Because trust law and SSI law about trusts are detailed and complex, we recommend that you discuss the matter with an estate attorney and SSA before taking any action to establish a trust.

Where You Can Live and Still Be Eligible for SSI

In order to be eligible for SSI benefits, you must live in the United States or in the Northern Mariana Islands (e.g., Saipan), which is a U.S. territory and be either a U.S. citizen or U.S. national or, as discussed below) in a non-citizen category that may qualify.

Even if you meet the other requirements for eligibility, the type of housing you have can make a difference in eligibility or payment amount. If your legal residence is a house, apartment, mobile home, hotel, cabin or other common type of residence, you can get SSI if your income and assets are within the limits.

You generally are not eligible for SSI if you reside for a whole month in a public institution such as a prison or public hospital where Medicaid is not paying the bill. The reason is that the government is already paying for your room and board. If Medicaid is paying at least half of the bill, you will be eligible for $30 a month if you have no other income.

You may be eligible if you live in any of the following:

- Publicly operated community residence with no more than 16 residents

- Public institution, to attend approved educational or job training classes

- Public emergency shelter for the homeless.

SSI Benefits May be Available to Certain Aliens

In addition to meeting all the other rules for SSI eligibility, including the limits on income and on resources, aliens may be eligible for SSI if they meet these two requirements: 1) Be in a qualified alien category; 2) Meet a condition that allows qualified aliens to get SSI.

Special Rules for Children of Military Personnel Living Overseas

Most people who receive SSI and leave the U.S. for 30 days or more (or the entire month of February) are no longer eligible for SSI payments. However, there is a special rule for the children of military personnel. They may continue to get SSI benefits or may apply for benefits while overseas if they are U.S. citizens and are living with a parent who’s a member of the U.S. Armed Forces assigned to permanent shore duty anywhere outside the United States.

If you’re such a parent and receive military orders to move overseas, and want your child(ren) to receive SSI benefits, contact your local Social Security office before you leave the U.S. and tell them:

- When you expect to report to your duty station overseas;

- When you expect your child(ren) to join you;

- Your mailing address at your new duty station; and

- Any details you can obtain about military allowances—e.g., housing allowances, rations allowances—at your new duty station.

If you’re already overseas and think your child(ren) may be eligible for SSI benefits, contact the nearest U.S. Embassy or Counselor O

fice, or write to:

Social Security Administration

Attn: SSI Military Children Overseas Coordinator

1 Frederick Street, Suite 100

Cumberland, Maryland 21502

Provide your current address, telephone number, and the Social Security number(s) of your child(ren). In addition to reporting changes in family income, assets, and living arrangement as they occur, also report if you leave the Armed Forces and remain overseas or your duty station changes.

Disabled or Blind Youth in Foster Care

If you are a disabled or blind youth about to be released from foster care because of your age —eligibility for foster care payments ends at age 18 in most states—you can apply for SSI payments three months early with an effective date of the first month you will no longer receive foster care assistance. You must be able to show that:

- You live in a foster care situation;

- You are blind or disabled;

- You likely will meet all of the non-medical eligibility requirements when foster care payments end; and

- You are within 90 days of losing foster care eligibility due to age.

Continuing Disability Reviews for Children

Once your child starts receiving SSI, SSA must review his/her medical condition from time to time to verify that he/she is still disabled. This review must be done at least every three years for children younger than age 18 if their condition is expected to improve. For babies who are getting SSI payments because of their low birth weight, the review must be done by age one, unless they have another medical condition shows that improvement is not expected by their first birthday. At each review, you must present evidence that your child has been receiving treatment that is considered medically necessary for his/her disabling condition.

If your child is receiving SSI payments when he or she turns eighteen, SSA will review his/her medical condition soon after he/she turns 18, using the adult disability rules to determine SSI eligibility. If your child was not eligible for SSI before his/her eighteenth birthday only because you and your spouse had too much income or resources, your disabled child may become eligible at age eighteen.

In Case of Dire Financial Need

If you need money right away due to a threat to your health or safety, for example, you do not have enough money for shelter, food, clothing, or medical care and you have been found disabled by SSA or are eligible for presumptive disability benefits, you may be eligible to receive an emergency advance payment or immediate payment form the local SSA office.

Can we get SSI if we have financial resources in excess of $2,000 for an individual or $3,000 for a couple?

Yes, you can get provisional payments if you agree to sell some of your countable assets, such as a house you don’t live in, a second car, a pleasure boat or highly valuable personal property. You can receive conditional SSI benefits after you sign an “Agreement to Sell Your Property” and SSA accepts it and you demonstrate that you are diligently trying to sell the named items. After they’re sold, you have to repay all of the SSI benefits you received during the time that you owned the property you were trying to sell. However, you will have had money to live on while you liquidate the property.

If I withdraw money from my bank account and loan it to somebody, thereby reducing my financial resources enough to qualify for SSI, is this OK?

It is okay to do so; however, if you’re reasonably certain you’ll be repaid, the amount of the loan would still be a countable resource. However, any interest you receive on the loan would not be counted.

Once I start receiving SSI payments, does the amount remain the same?

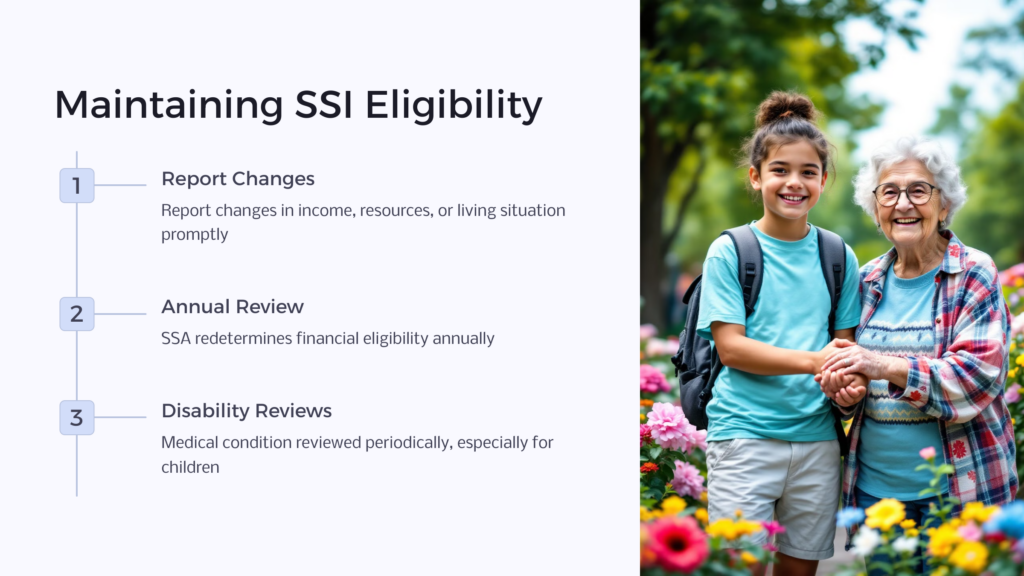

No, benefits are calculated monthly and can change monthly. You are required to report changes in income, resources, or residence or changes in the people who live with you or other factors that determine payment amount. Reports should be done by the tenth of the month after the month in which the change occurs if the report is made in person and by the eighth if made by telephone. Additionally, SSA usually redetermines your financial eligibility once a year in a comprehensive review. If unreported changes have occurred, the redetermination could result in your being either overpaid or underpaid.

What are the potential penalties for SSI fraud?

Potential penalties include fines and/or imprisonment and, of course, a stop to SSI payments.

What’s considered fraudulent?

Any act or omission that falsifies or hides information with the intent of concealing the information. Also, using someone else’s benefits for oneself—including a representative payee using the SSI recipient’s benefits for anyone or anything other than the disabled recipient—may be fraud.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.