Social Security back pay refers to retroactive benefit payments you may receive after your Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) claim is approved. These payments compensate you for the time between your disability onset or application date and the date your claim is approved, reflecting the lengthy processing times often involved in disability claims.

SSDI back pay includes a five-month waiting period and may include retroactive benefits for up to 12 months before your application date. SSI back pay, on the other hand, generally begins with the first full month after your application date. The calculation differs significantly between the two programs and can become especially complex in concurrent claims involving both SSDI and SSI.

Why This Update

Social Security benefits are adjusted annually through Cost-of -Living Adjustments (COLA), which may affect the amount of back pay owed for prior years, including 2026.

Social Security Back Pay

Social Security back pay provides retroactive disability benefits for people applying for Social Security Disability benefits for SSDI and SSI. It covers the period from your established disability onset or application date until your claim is approved. The purpose is to compensate for the often lengthy processing times of disability applications.

SSDI Back Pay

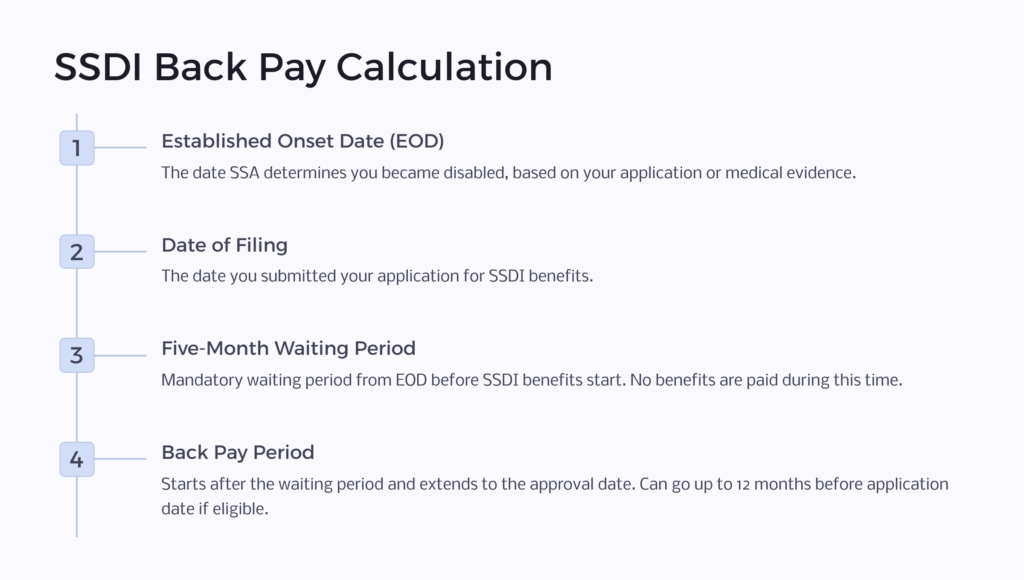

SSDI back pay is calculated using your Established Onset Date (EOD) and the date you filed your application. The EOD is the date the Social Security Administration (SSA) determines your disability began based on the medical evidence in your file. This date is important because the mandatory five-month waiting period begins on the EOD.

You will not receive SSDI benefits during the five-month waiting period. After the waiting period ends, back pay begins accruing and continues through the date your claim is approved.

Your monthly SSDI benefit amount is generally based on your lifetime earnings history, although COLA increases or certain offsets may affect the amount during the retroactive period. The longer the processing time after the waiting period ends, the larger your potential back pay award may become.

Typical Timelines and Amounts

SSI back pay generally begins with the first full month after your application date or the date you became financially eligible, whichever is later. Unlike SSDI, SSI does not have a five-month waiting period.

Large SSI back-pay awards that exceed three times the maximum monthly federal benefit rate are typically paid in installments. This process may help protect eligibility for other means-tested benefits by preventing a large lump-sum payment from immediately counting as a resource. However, SSA may issue larger lump-sum payments in certain situations involving financial hardship or urgent needs.

State supplementary payments and any interim assistance provided by a state agency may also affect the total SSI back-pay amount. If you received state assistance while awaiting your SSI decision, the state may be reimbursed from your back pay.

Concurrent Claims: SSDI and SSI Back Pay Together

Concurrent claims involve potential eligibility for both SSDI and SSI benefits, which can lead to complicated back-pay calculations.

SSDI back pay may reduce or offset SSI back pay because SSDI counts as income under the needs-based SSI program. In many concurrent claims, SSA calculates SSDI retroactive benefits first and then treats those payments as income when calculating SSI benefits for overlapping months.

As a result, retroactive SSDI payments may reduce SSI eligibility during certain months and could lead to offsets or overpayment adjustments. Despite the coordination between the programs, SSDI and SSI back-pay awards are generally issued separately, and you may receive separate notices and payments for each benefit program.

Example Scenario

If you applied for SSDI benefits last year and your claim was recently approved after a lengthy review, you might be expecting back pay.

One veteran discovered that their approved Established Onset Date (EOD) was several months before their application, potentially qualifying them for retroactive benefits and payments covering the processing period, after the initial waiting period.

Legal representation can help ensure you receive every dollar you’re entitled to in back pay. Disability attorneys typically work on a contingency-fee basis, meaning you pay a fee only if you win your case. This fee is usually deducted from your back pay in accordance with SSA guidelines.

Frequently Asked Questions

What is the difference between SSDI and SSI back pay?

SSDI back pay is based on your work history and your Established Onset Date, and it includes a mandatory five-month waiting period. In some cases, SSDI benefits may be paid retroactively for up to 12 months before the application date.

SSI back pay is based on financial need and generally begins with the first full month after the application date. SSI does not include a waiting period.

Is there a waiting period for Social Security disability back pay?

Yes. SSDI includes a mandatory five-month waiting period beginning on your Established Onset Date (EOD). No SSDI benefits are payable during this period.

SSI does not have a waiting period.

How far back can SSDI back pay go?

SSDI back pay may include retroactive benefits for up to 12 months before your application date if SSA determines you were disabled during that period.

How is SSI back pay issued?

If your SSI back-pay award exceeds three times the maximum monthly federal benefit rate, SSA will typically issue the payments in installments. Smaller amounts may be paid in a single lump sum.

Can receiving SSDI back pay affect my SSI benefits?

Yes. If you qualify for both SSDI and SSI, retroactive SSDI payments may count as income for SSI purposes and could reduce the amount of SSI back pay you receive.

SSI recipients should also understand that back-pay funds may eventually affect SSI resource limits if the money is retained beyond the allowable exclusion period.

What is an Established Onset Date (EOD)?

The Established Onset Date (EOD) is the date SSA determines your disability began based on the medical evidence in your case. This date is critical because it determines when the SSDI waiting period begins and how much back pay you may receive.

Should I get a lawyer to help with my back pay calculation?

Although legal representation is not required, consulting with a Social Security disability lawyer or advocate can be beneficial, especially in complex cases or concurrent claims.

Attorney fees are generally deducted from your back pay under a fee agreement, and SSA typically caps fees at 25% of past-due benefits up to a maximum amount set by the agency.

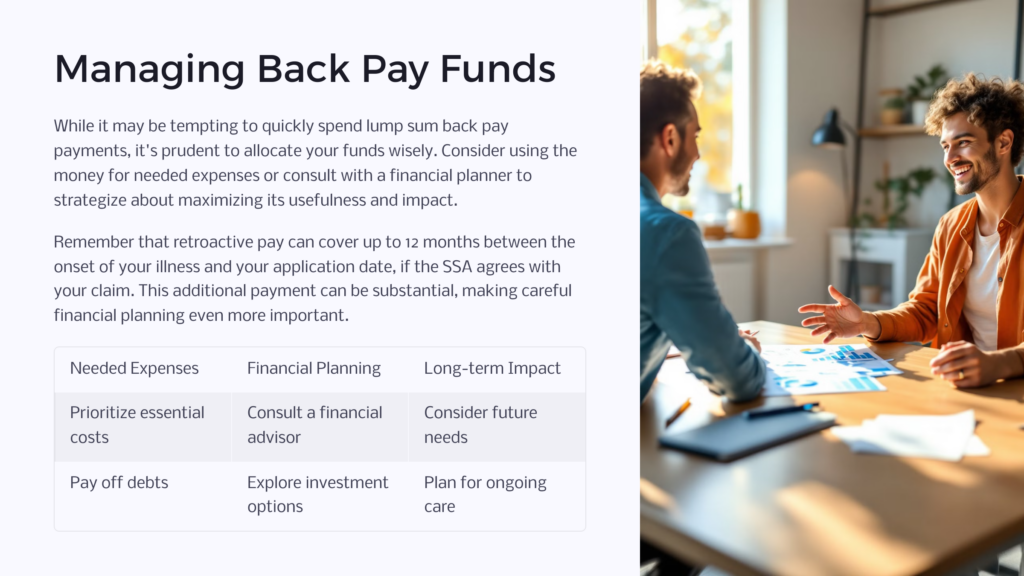

Maximizing Your Back Pay and Managing Funds

You should apply for Social Security disability benefits as soon as it becomes clear that your condition is expected to prevent substantial work for at least 12 months or result in death. Delaying your application may reduce the amount of retroactive SSDI benefits you can receive.

Keep in mind that receiving a large lump-sum payment could affect eligibility for other means-tested benefits such as Medicaid or housing assistance. Although retroactive SSDI and SSI payments are generally excluded from SSI resource calculations for nine months after receipt, those funds may become countable resources afterward if they are not properly managed.

Carefully planning how you use your back pay may help protect future eligibility for benefits and improve long-term financial stability.

If you still have questions about your back pay or whether you may qualify for disability benefits, Benefits.com can guide you through the process and help you better understand your options!

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.