California’s disability benefits system—often just called State Disability Insurance, or SDI—exists to support those who’ve temporarily lost their ability to work. Think of it as a safety net; when life’s unpredictability hits you (like injuries or illnesses), the California State disability insurance system can step in to provide an emergency disability benefit payment.

If you’re unable to perform your regular work for a medical reason—and your doctor agrees—you’re likely considered “disabled.” But to be qualified for State Disability insurance benefits, the disability must be non-work-related. If it’s an injury or illness tied to your job, then you should go through Workers’ Compensation instead.

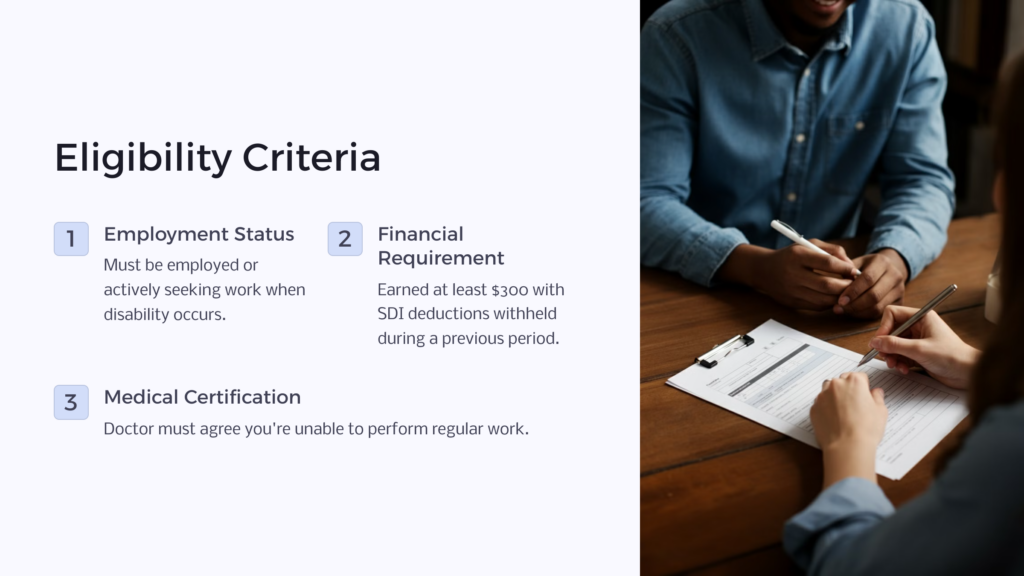

Eligibility Criteria for Applicants

Just like Social Security Disability Insurance (SSDI), in order to qualify for California State Disability Insurance, there are a few boxes you’ll need to tick. First, you must be employed or actively seeking work when you become disabled. So if you’re lounging on the couch and haven’t been job-hunting, it’s a no-go. But if you’ve been working or actively job-hunting, then you’re on the right track.

Next, there’s a financial aspect. You’ve got to have earned at least $300 from which State Disability Insurance (SDI) deductions were withheld during a previous period. Basically, if you’ve been working and SDI was taken out of your paycheck, you’re probably set. Other factors include how long you’ve worked, if you’re under medical care, or if you’re experiencing simultaneous unemployment benefit payments.

Short Term vs. Long Term Disability Benefits

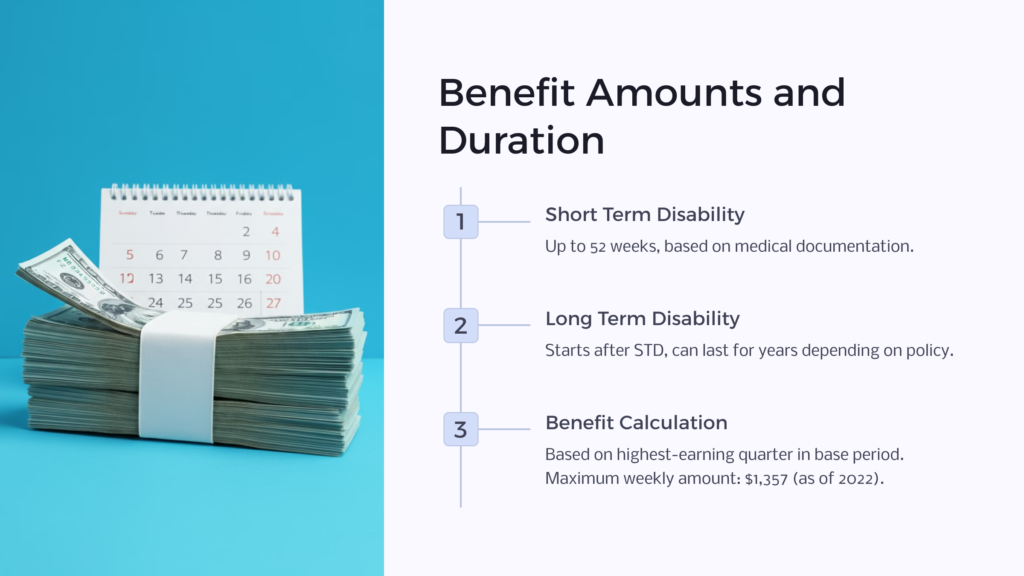

Short term disability benefits (STD benefits, not to be confused with SDI, or State Disability Insurance) kick in when you’re temporarily unable to work. Imagine spraining an ankle or catching a severe flu—events that knock you off your feet, but won’t last forever. Generally, STD benefits in California can last up to 52 weeks, but the exact duration often hinges on the medical info provided.

Long term disability (LTD) benefits apply when the medical situation is more permanent. Serious conditions—heart disease, mental health challenges, certain types of cancer, etc.—can fall under this category. LTD doesn’t kick off instantly; there’s a waiting period after your short term benefits run out.

Also, while STD is state-managed, LTD often comes from private insurance. So, while they work hand-in-hand, you should make sure you’re meeting the requirements of both parties.

Duration and Limits of Disability Coverage

For STD, you could be looking at up to 52 weeks of disability benefit payments. But that’s assuming your medical documentation supports this duration. It’s not a fixed period; it’s more of an “up-to” 52 weeks, but could be any number of weeks below that.

LTD typically starts after STD runs its course and can last for years, depending on the policy’s terms. Some policies might cover you for a set number of years, while others might extend until retirement age or even for life. Again, it varies based on the policy specifics and the nature of your disability.

Determining Benefit Amounts

How much can you expect to get in your SDI payment? It’s not a one-size-fits-all answer; the benefit amount hinges on a blend of factors. The most prominent one is your past earnings—getting repaid with some of what you’ve put into SDI deductions from your paycheck.

The State of California takes an average of your highest-earning quarter in a defined base period—typically 12 months before your disability. This average is then used to calculate your weekly benefit amount. But hold on, there’s a cap! As of my last update in 2022, the maximum weekly amount is around $1,357. Still, most folks get about 60-70% of their usual salary.

A couple of other things can affect your benefits—like other income sources or if you’re able to work part-time. But the gist is this: the goal is to partially replace lost wages, ensuring you stay afloat during tough times.

Tax Implications of Disability Payments

For the most part, in California, state disability benefits are considered taxable income by the federal government, so expect taxes from the federal government. However, California doesn’t tax SDI benefits at the state level—just the federal government.

What about private long term disability insurance? The benefits typically aren’t taxable if you paid your insurance premiums with after-tax dollars. Conversely, those benefits might be taxable if your employer footed the bill or used pre-tax dollars.

Medical Documentation: What’s Required?

A licensed physician or a qualified medical professional must certify your disability. Documents for this process usually include details about your condition, its severity, and an estimation of how long you’re expected to be out of commission.

Consistent follow-ups with your healthcare provider are often required to maintain your benefits. Think of it as a periodic check-in, ensuring everything is on track and aligning with the initial prognosis. Plus, these regular updates identify if/when a return to work is feasible.

Appealing a Denied Disability Claim

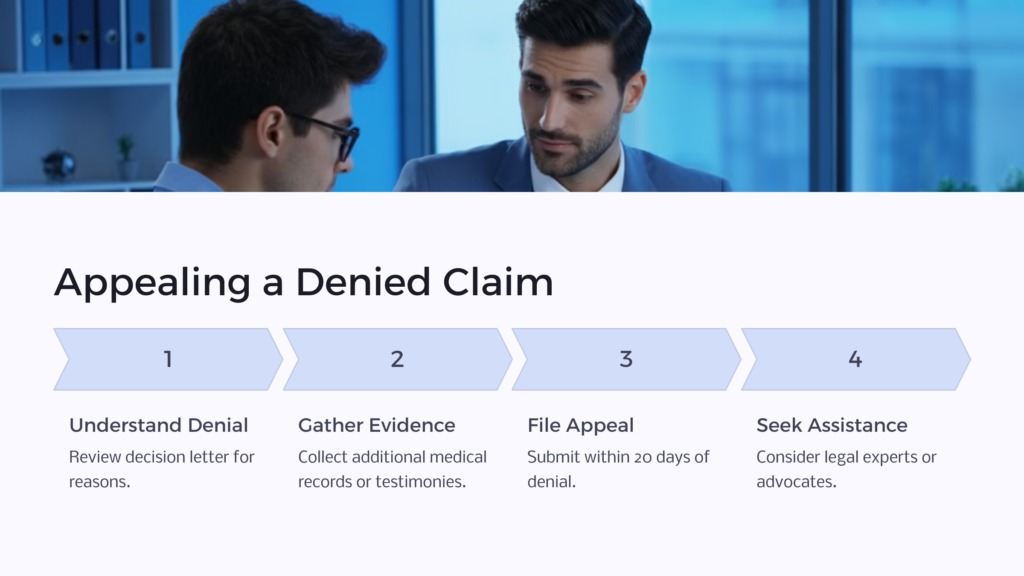

If your disability claim gets denied, it’s disheartening, but it’s not the end of the road. There’s an appeal process in place, and you’ve got rights.

When you receive a denial, the first step is to understand why. The reason for denial is typically outlined in the decision letter. From there, you’ve got a limited window—usually about 20 days—to appeal the decision.

Gathering additional evidence can be your ace in the hole. This might mean more medical records, specialists’ letters, or even colleagues’ testimony about how your disability affects your work. It’s crucial to be thorough, timely, and persistent. And remember, seeking assistance—from legal experts or advocates—can often tip the scales in your favor.

Frequently Asked Questions about CA Disability

While designed to be supportive, disability benefits can sometimes feel like a maze of regulations, terms, and procedures. Let’s tackle some of the most common queries about CA Disability.

1. How Soon Can I Get Benefits After Applying?

Once you’ve submitted your application—and assuming all documentation is in order—you could start seeing payments as early as two weeks. But remember—timeliness largely depends on the accuracy and completeness of your application.

2. Can I Work While Receiving Disability Benefits?

Yes, but there’s an “earnings ceiling” that may result in you receiving a lower benefit amount if you earn more than a certain amount.

3. What if I’ve Moved out of California?

Even if you’ve moved out of state, as long as you earned your wages in California and meet the other eligibility criteria, you can still apply for and receive CA Disability benefits.

4. Do Pregnancy and Childbirth Qualify for Benefits?

Yes. Many mothers take advantage of benefits during their maternity leave as they recover from pregnancy and childbirth complications.

5. How is the Benefit Amount Calculated?

Your benefit amount is determined by your past earnings, specifically looking at a base period before your disability began. The state will calculate an average based on this and provide you with a percentage of that average as your weekly benefit.

6. What’s the Maximum Duration for these Benefits?

For short term disability, the maximum duration is typically up to 52 weeks. However, the actual duration will hinge on your medical documentation and the nature of your disability.

7. Do I Need to Regularly Update the State about my Condition?

Yes, regular medical evaluations are essential to ensure you continue to qualify for benefits. Plus, these updates can determine if adjustments to your benefits are needed or if a return to work is on the horizon.

Is Private Insurance Right for Me?

We recommend that, when possible, you should apply for both private insurance and state benefits. Here are some points that private insurance covers but that state insurance may not:

1. Coverage Gap

CA state disability typically covers 60-70% of your income. Private insurance can supplement this, offering closer to full salary protection.

2. Benefit Duration

State disability benefits generally last up to 52 weeks. Private long-term policies can extend coverage for years or up to retirement.

3. Customization

Private policies often provide tailored features like specific riders or cost-of-living adjustments.

4. Cost Implications

While offering more extensive benefits, private insurance comes with premiums. Assessing their affordability is crucial.

5. Occupation-Specific Risks

Private insurance can offer specialized coverage for those in high-risk or physically demanding jobs, considering profession-specific vulnerabilities.

6. Flexibility

Private disability benefits typically have fewer restrictions, allowing more freedom in using funds.

7. Additional Security

Private insurance is an extra financial buffer, providing enhanced protection against unforeseen challenges.

Understanding Other Issues

Fraud

Fraud in the disability benefits system occurs when an individual knowingly provides false information, omits crucial details, or misleads the authorities to gain undeserved benefits. Such actions not only jeopardize the individual’s current and future claims but also strain the resources meant for those genuinely in need. For instance, someone might exaggerate their condition, continue to claim benefits while working covertly, or use someone else’s identity to file a claim.

The consequences of such deceit can be severe. It can lead to disqualification from the program, mandatory repayment of unduly received funds, hefty fines, and in extreme cases, legal prosecution. Beyond the tangible penalties, committing fraud tarnishes one’s reputation, making future financial or job-related endeavors more challenging.

Overpayment

On the other side of the spectrum is overpayment, a situation where beneficiaries receive more funds than they’re entitled to. Unlike fraud, overpayment doesn’t always stem from malicious intent. Sometimes, it’s due to administrative errors, delayed reporting of changes in one’s medical or employment status, or misunderstandings about eligibility requirements. However, regardless of its cause, overpayment is a debt that must be repaid.

If you ever find yourself in an overpayment situation, it’s crucial to act promptly. Informing the concerned authorities, understanding the cause of overpayment, and setting up a repayment plan can mitigate potential repercussions. Remember, while inadvertent overpayment is not fraudulent by nature, intentionally not reporting it can cross into the territory of deceit.

You Don’t Have to Do it Alone

Benefits.com offers free counseling to help clarify the process, answer questions, and steer you toward the right choices. Don’t leave your benefits to chance; get informed, empowered, and confident in your decisions. Connect with us today and secure the support you rightfully deserve.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.