Most American workers are aware that if they participate in the workforce and pay into the Social Security tax system, they are also eligible to draw benefits when they choose to retire if they meet certain age criteria. But a lesser known fact is that spouses who did not work outside the home throughout their lifetime also are eligible to receive a Social Security payment in the form of the spousal benefit.

These are partial retirement benefits granted to the spouses of qualifying taxpayers. If this is news to you, keep reading – it’s important to understand all of your retirement income options, so we’ve outlined everything you need to know about claiming spousal benefits.

10 Important Facts About Social Security Spousal Benefits

- Length of marriage is important

- You may be eligible for up to half of your spouse’s retirement benefit amount

- Other benefits could reduce spousal benefits

- You must wait until your spouse collects benefits before claiming spousal benefits

- Length of marriage is important

- It’s possible to claim spousal benefits even if you also worked yourself

- You can claim spousal benefits even if you’re divorced

- Widows and widowers can claim spousal benefits

- Age matters

- Spousal benefits don’t grow by deferment

Social Security spousal benefits can be a major financial help during retirement, whether you never worked at all or if you worked but weren’t the higher earner in your household – so it literally pays to familiarize yourself with how spousal benefits work. In general, the Social Security Administration allows a non-working spouse to draw a maximum spousal benefit equal to 50 percent of the higher-earning spouse’s Social Security retirement benefit amount, though there are some parameters you should be familiar with.

Before you decide to apply for Social Security spousal benefits, make sure you’re clear on your specific situation, along with all the qualification criteria. Don’t leave money on the table by failing to research your options to decide what makes the most sense for you. Luckily, the guidelines around spousal benefits are pretty clear and straightforward. To help you get started, we’ve outlined some of the major must-know facts about what it takes to qualify for Social Security spousal benefits.

There are several important things to keep in mind when claiming spousal benefits – the key points are outlined below.

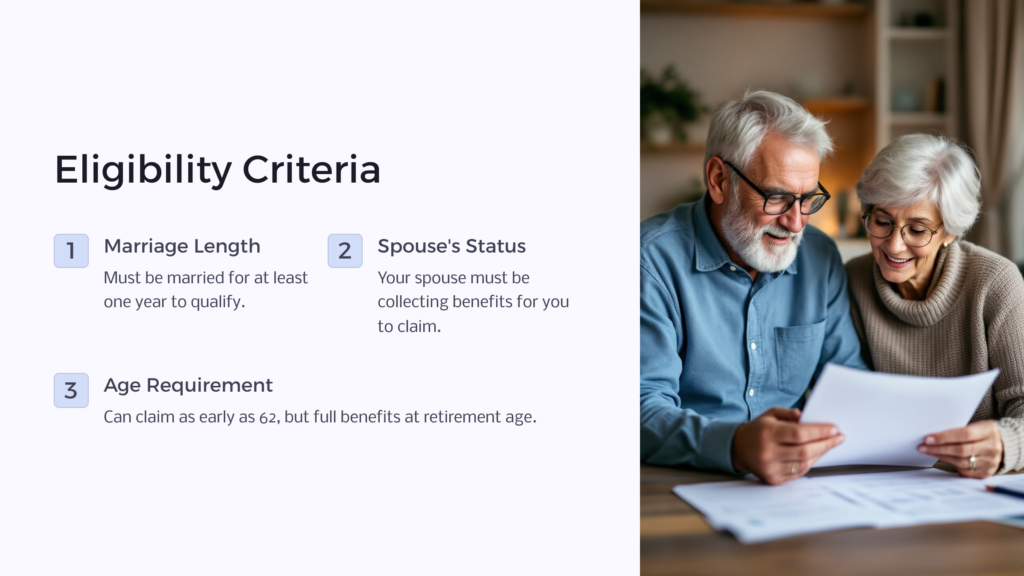

1. Length of Marriage is Important

You must be married to your current spouse for at least one year to be eligible for Social Security spousal benefits. There are a couple of exceptions to this rule, though. If you marry someone who is the biological parent of your child, the one-year waiting period can be waived. Also, if you were entitled to Social Security benefits based on someone else’s work record in the month before you married, the SSA will waive the one-year waiting period.

Situations like this include existing spousal benefits, a survivor’s benefit, or parents’ benefits. For example, if you were already eligible for spousal benefits based on the earnings of a former spouse, then remarried, you’d immediately be eligible for spousal benefits based on your new spouse’s earnings, with no one-year waiting period.

2. Other Benefits Could Reduce Spousal Benefits

If you’ve never worked outside the home, Social Security spousal benefits are likely your best chance of receiving any type of Social Security income once you reach your full retirement age. However, if you receive benefits from a government pension or income from a foreign organization or entity not covered by Social Security, those benefits can reduce the amount of income you can receive from Social Security. You may still be eligible to receive spousal benefits, you’ll just receive a limited benefit rather than one calculated at the full 50% rate.

3. You May Be Eligible for Up To Half Of Your Spouse’s Retirement Benefit Amount

Even if you never worked yourself, you may be eligible to draw benefits based on your spouse’s work record, as long as he or she is eligible for Social Security retirement benefits. In fact, you’re likely eligible to claim 50% of your spouse’s Social Security retirement benefits amount at his or her full retirement age. For example, if your current spouse is eligible for a $1200 monthly Social Security payment at full retirement age, you would be eligible for a $600 monthly Social Security benefit at your full retirement age.

But keep in mind that, just as with conventional Social Security benefits, you only get the full amount if you wait until your full retirement age. While you can file for spousal benefits as early as age 62, you’ll get less than your full benefit amount at that point. It makes sense to wait, if possible, until your full retirement age before claiming your spousal benefits.

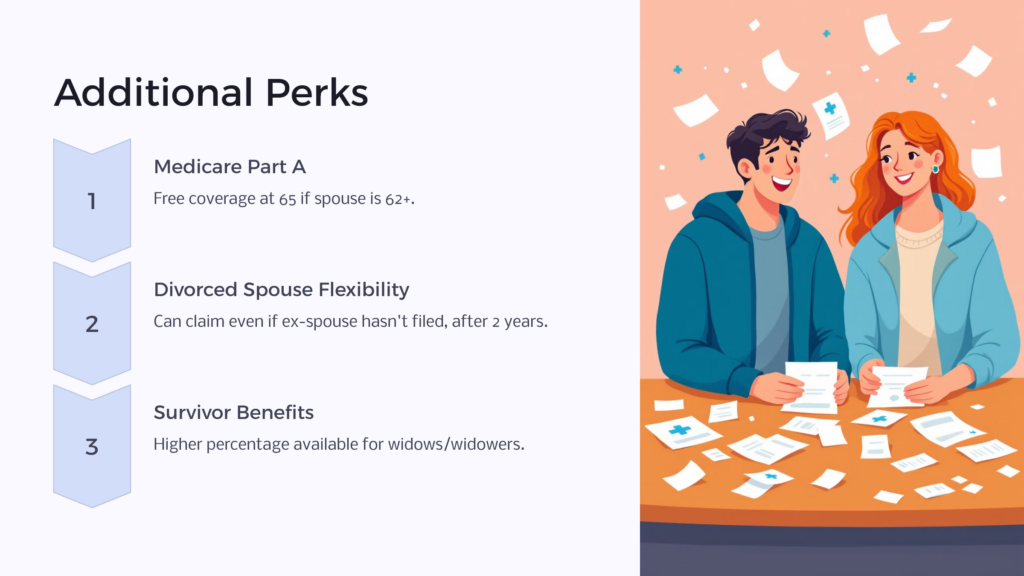

There’s another benefit you might consider: Not only are you entitled to an amount equal to 50% of your higher-earning spouse’s benefit, but you also are eligible to free, premium Medicare Part A coverage when you reach age 65. There’s one catch, though – your spouse must be at least age 62 for you to qualify for this benefit. So, if you’re more than three years older than your spouse, you may need to purchase your own Part A policy until your spouse reaches age 62.

4. You Must Wait Until Your Spouse Collects Benefits Before Claiming Spousal Benefits

Even if you’re eligible for spousal benefits, you have to wait until your spouse files to receive benefits before you can receive any money based on his or her work record. If your spouse keeps working after retirement at a lowered capacity, yet doesn’t choose to begin collecting Social Security retirement benefits, you must wait as well. But if you’re eligible for Social Security retirement benefits based on your own work record, you can go ahead and begin receiving those. If your Social Security spousal benefit amount is higher, you get to bump up to that amount once your spouse begins receiving benefits.

This is a relatively recent change to the guidelines around spousal benefits. Until 2016, a working spouse could file for benefits, then suspend receipt of them, which would allow a non-working or lower earning spouse to begin collecting spousal benefits early. But that loophole was closed with the Bipartisan Budget Act of 2015, which went into effect in April of 2016.

5. It’s Possible to Claim Spousal Benefits Even If You Also Worked Yourself

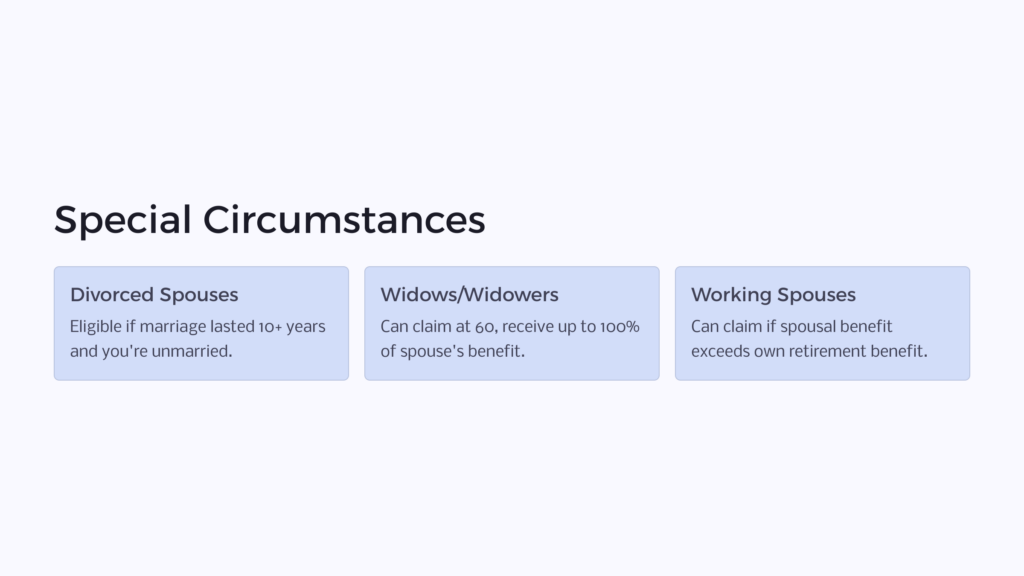

This may come as a surprise, but spousal benefits aren’t limited to those who have never worked outside the home. If you are entitled to Social Security retirement benefits related to your own work history, but those benefits amount to less than half your spouse’s benefit at full retirement age, you can then claim a spousal benefit and take the higher benefit income.

This may come as a surprise, but spousal benefits aren’t limited to those who have never worked outside the home. If you are entitled to Social Security retirement benefits related to your own work history, but those benefits amount to less than half your spouse’s benefit at full retirement age, you can then claim a spousal benefit and take the higher benefit income.

One key point to remember, though, is that you aren’t allowed to double dip – you can’t claim your own retirement benefit and also claim your spouse’s. But you can choose to receive the benefit that gives you the highest amount of income. Only one spouse per household is eligible to receive spousal benefits. Most women who work and are thus eligible for their own benefits end up taking their Social Security retirement benefits because the payments are more than 50% of their spouse’s benefit amount.

6. You Can Claim Spousal Benefits Even If You’re Divorced

You don’t have to be currently married to qualify for spousal benefits. If you were married to your divorced spouse for at least 10 years and you haven’t remarried, you’re entitled to benefits based on your ex-spouse’s work record.

Also, if you’ve been divorced for at least two years, you can even claim spousal benefits if your spouse hasn’t begun receiving Social Security retirement benefits – if you’re at least age 62. This is an exception to the usual rule of having to wait for your spouse to claim benefits before you can claim spousal benefits.

If you have remarried, you are no longer eligible for Social Security spousal benefits based on the earnings of your former spouse. You also aren’t eligible if you receive benefits on your own that are greater than 50 percent of your ex-spouse’s benefit amount at full retirement age.

7. Widows and Widowers Can Claim Spousal Benefits

If your spouse is deceased, you may still be able to qualify for Social Security spousal benefits if a few key facts are true. First, the surviving spouse and the deceased spouse must have been married for at least nine months. If this is the case, once you reach age 60, instead of receiving half your spouse’s full retirement benefit amount, you can receive 71% of their earned benefit amount. Or you can wait and receive 100% of their earned benefit amount when you file at your full retirement age. This is a rare case when a benefit is available before age 62.

8. Age Matters

You can begin drawing Social Security spousal benefits as early as age 62. As with traditional retirement benefits, you won’t receive your full benefit amount unless you wait until your full retirement age, which is typically age 66 or 67 for most workers today. In order to get the highest possible benefit payment, you should wait, if possible, until your full retirement age before beginning to collect your Social Security spousal benefits.

9. Spousal Benefits Don’t Grow by Deferment

With traditional Social Security benefits, the longer you wait to claim them, the higher your benefit amount will be – up to age 70. But that’s not the case with spousal benefits. Instead, there’s no benefit to waiting beyond full retirement age to claim spousal benefits. Your benefit amount will not grow by waiting to take it beyond this point like it would for your own delayed retirement. So, make sure that once you reach your full retirement age, you begin claiming your spousal benefits as soon as possible.

Social Security Spousal Benefits

Spousal benefits provide for the spouse who stayed home during a marriage instead of working. By claiming Social Security spousal benefits, you can ensure that your retirement years are not severely limited by a lack of income. For more than 80 years, Social Security retirement benefits have helped the quality of life for millions of American retirees.

A recent Social Security study showed that roughly 2.3 million Americans received at least some part of their Social Security retirement benefits as the spouse of a qualified taxpayer. If you’ve ever been married, you may qualify for Social Security spousal benefits. These benefits are an important income supplement for many retirees.

Benefits.com Advisors

Benefits.com Advisors

With expertise spanning local, state, and federal benefit programs, our team is dedicated to guiding individuals towards the perfect program tailored to their unique circumstances.

Rise to the top with Peak Benefits!

Join our Peak Benefits Newsletter for the latest news, resources, and offers on all things government benefits.